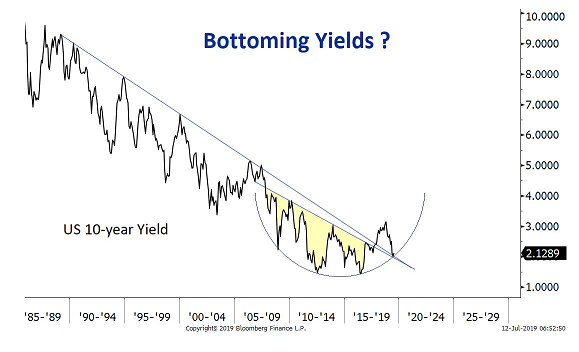

La stampa in Italia ha tenuto, su questa vicenda, un profilo bassissimo: lo spazio che è stato dedicato alle vicende di H2O, di Woodford e di GAM è ad oggi pochissimo. E tutti gli interventi che abbiamo letto (ci scusiamo se ne avessimo mancati alcuni) sono impostati come interventi di “pompieraggio”, il cui scopo è buttare acqua sul fuoco, minimizzare, e ridurre la portata di questi fatti. “Tutto normale” e “nulla di grave” sono i messaggi che traspaiono da questi articoli.

Nel resto del Mondo, invece, alcuni media hanno assunto un atteggiamento diverso.

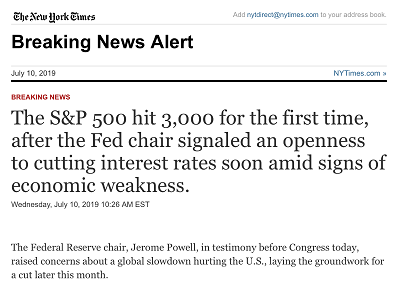

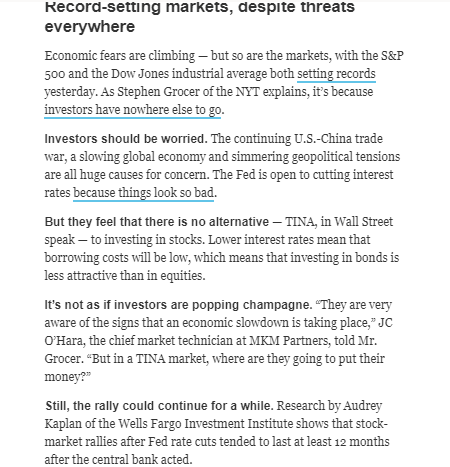

Per questo, ed anche allo scopo di non ripeterci con frasi che avete già letto, riportiamo oggi per intero un articolo apparso in settimana sul Financial Times, la cui lettura mette ogni cosa al suo posto. Nel senso che spiega perché è falso affermare che “tutto è normale” e che “non è successo nulla di grave”, oppure peggio ancora affermare che “non è stato fatto nulla di irregolare”. Una lettura che vi sarà utilissima e cui si riferisce il commento che leggete in apertura di Post, ed anche l’immagine che lo accompagna, che ricorda a tutti le code fuori dalle Filiali di Northern Rock, nel Regno Unito, dieci anni fa.

Recce’d per ora si ferma a questo. Ma c’è da essere sicuri che i fatti dei prossimi mesi ci porteranno a riparlarne diffusamente.

At this point, following Fleet Street form, coverage of funds at H2O and similar institutions should degenerate into a minute examination of lifestyle choices and blurred images showing over-the-top spending and people having a good time.

However, one sentence apparently said by someone in authority at H2O tells a much bigger story: “Questioning the liquidity of our funds is equivalent to ascertaining the incapability of a bank to refund its deposits, with the devastating consequences which history has taught us.” This reads like a letter composed of words cut out from newspapers and pasted into a message sent to police: “STOP ME BEFORE I DISINTERMEDIATE AGAIN!!!” Strictly speaking, H2O is not a bank and does not accept deposits. Asset managers’ portfolio liquidations are not bank runs. The industry does not have systemic oversight by bank regulators or central banks. Of course, neither I nor the Financial Times take any view on the legal exposures of portfolio managers whose funds have been subject to rapid withdrawals. As one US asset manager said: “I would not say that whoever put that out should be fired but they connected dots that should not be connected. The other thing is that it has become obvious that some in the portfolio management industry desperately want to become banks, so they can have direct access to the Fed window or other central bank channels for repurchase agreement funding and non-market sources of immediate liquidity. “The turnround time on liquidating a mutual fund, an ETF or a Ucits fund can stretch into weeks or months. That is too much maturity transformation unless you have access to the backstop (ie, a central bank). The only way to be given access to the backstop is if you are too big to fail and have the public on your side.”

In the old days, more than a decade ago, our manager’s backstop might have been a bank’s provision of expensive, embarrassing but immediate cash. Now, given the more complex plumbing of derivatives trading, the shortage of high-quality liquid assets in much of the world and less cross-border amity, the cash would have to be supplemented by good collateral, that is, Bunds and US Treasury securities, perhaps accompanied by currency swap lines. To get that sort of help, you really need to be too big to fail or be part of a group that has been so designated. Looking at the political scene these days, it is not easy to find decisive, well-informed leaders ready to take the hard decisions when necessary. In a crisis, though, a few opportunists may be enough. After all, there were some unimpressive people in charge in 2008 but a course of action was patched together (or stitched up). A few of those veterans are ready to be repurposed for the next task of a global bailout and legitimising regulation for the asset management industry. Some US asset managers, the sort with bronze eagles on their desks and photos of themselves with the president, may have moral objections to more federal or international regulation.

If the call centres are swamped due to dedication to principles, though, maybe some new principles are needed. When the requirement for the new asset management regulations and liquidity arrangements becomes really obvious, some in the industry will have plans ready. Of course, their scheme will be best suited to big firms but consolidation was coming one way or another. As one of the heads of those big firms told me recently: “While we have more tools in the box, such as (withdrawal) gates and swing pricing, there is no denying we have a looming liquidity crisis. It has been masked by the profligacy of the central banks in the past decade. “Because we no longer have the banks doing market-making, we have created the conditions for liquidity mismatching. We need to do better analysis of both sides of the balance sheet and not confuse listed assets with liquid assets, since in a crisis, liquidity and even pricing is uncertain. We need to have a buffer of cash plus high-quality liquid assets. “Tensions will concentrate in the retail space of portfolio management because it is more volatile.

That is why the regulators will have the scope for taking action. It has been a mistake to deny the potential systemic effects of our current structure. Those have been poorly researched, specifically on the channels of transmission of [systemic shocks]. “Also, there is a need to incentivise the asset managers to run a balance sheet at the corporate level. This has been an undercapitalised industry.” Just how quickly, though, could any global bailout/re-regulation of asset managers be effected? I think it depends on how many millions of retail customers get a shock when they try to cash in or transfer assets, or when they get surprising monthly statements. Then it is quite possible no one will want to take more than a couple of months to come up with a common plan for prudential regulation, and, by the way, direct access to central bank liquidity and currency facilities for asset managers