Nella prima parte di questo secondo Longform’d (che abbiamo deciso di dividere in due parti per facilitarne la lettura) abbiamo scritto che per comprendere la realtà di oggi, sui mercati finanziari internazionali, è necessario:

guardare al di là delle Borse, ai mercati obbligazionari, valutari e delle materie prime

comprendere a fondo, e nel dettaglio, le azioni delle Banche Centrali, ed il loro ruolo (che è passivo, e non attivo) in questa fase dei mercati

fare non uno, ma quattro passi indietro, e riesaminare la situazione a partire dai primi giorni del 2019

Per questa ragione, Recce’d vi ha accompagnato lungo un percorso in quattro punti, l’ultimo dei quali è la svolta del mese di agosto 2020 in casa della Federal Reserve.

La seconda parte del secondo Longform’d, che state leggendo, vi chiede di ritornare indietro di un passo, lungo quel percorso, dall’agosto del 2020 al marzo del 2020.

Siamo sicuri che la gran parte dei lettori ha dimenticato la maggior parte dei fatti del marzo 2020, e se interrogata a proposito risponderebbe raccontando soltanto i crolli di Borsa.

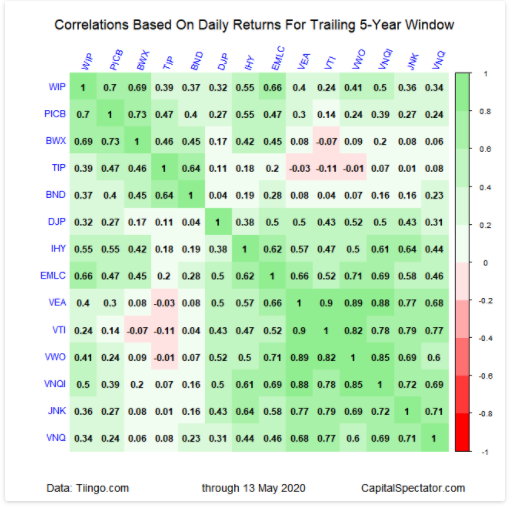

In realtà, il fatto più clamoroso di quel mese di crisi fu la sostanziale paralisi dei mercati dei Titoi di Stato, documentata da noi con le due immagini che avete appena visto.

Tra di voi, molti se ne sono (comprensibilmente) dimenticati, a causa dell’intensa campagna di mal-informazione delle Reti di vendita, delle TV come CNBC, e delle pubblicazioni delle cosiddette banche di investimento.

E di certo, non vi ha aiutati a ricordare questi fatti il vostro venditore di fiducia, che voi chiamate magari wealth manager oppure private banker oppure consulente addetto alla vendita.

Noi invece vi aiutiamo a ricordare i fatti di sette mesi fa: leggiamo, al proposito, un articolo della metà di marzo 2020.

Amid frenzied trading over the past week, the $18 trillion U.S. Treasury market showed cracks that raised eyebrows across Wall Street, and finally led the Federal Reserve to announce a range of measures on Sunday night including purchases of hundreds of billions of U.S. government bonds over the coming months.

Market participants say the cost to trade Treasurys with virtually identical terms but which differ in maturities by a few months has diverged sharply last week as traders struggled to buy and sell bonds in a hurry. This worrisome phenomenon underlines how volatility across Wall Street has seen trading volumes for older Treasurys slump even in the U.S. bond-market which is advertised as the deepest and most liquid safe-haven asset in the world.

“I have never seen moves like this in 35 years of trading. I’ve never seen anything like it. At this point, the market will get absolutely exhausted,” said Tom di Galoma, managing director of Treasurys trading at Seaport Global Securities.

See: Fed shifts policies to ease ‘highly unusual disruptions’ in Treasury financing markets

Iceberg

The U.S. Treasury market is much like an iceberg.

The more visible and most widely traded part of the market are newer “on-the-run” securities which are the bonds most recently issued by the U.S. government, but it’s the older “off-the-run” securities that represent the bulk of the $18 trillion market. Much of it is held by fund managers, insurance companies, pension funds, and other investors who buy government bonds to earn a steady stream of income.

After the government sells a new round of bonds to investors, those recently issued securities become the new on-the-run securities, relegating the older issues to so-called off-the-run status.

Though traders have been able to move in and out of on-the-run Treasurys with relative smoothness, it’s the less liquid and much bigger off-the-run portion of the market that has seen a sharp erosion of liquidity. This has led to a sharp widening of the price difference between the two buckets of bonds, know as the basis, in recent sessions.

The surge in trading costs for older off-the-run Treasurys highlights the enormous pressure faced by broker-dealers, the middlemen of the bond-market, who are grappling with the biggest swings in government debt yields in sometimes decades.

“If we can’t price and clear Treasurys in a very efficient manner, the market is going to have broader issues,” said Gregory Faranello, head of AmeriVet Securities.

In calm trading, the difference in prices between newer and older Treasurys is usually slim.

That’s because textbook financial theory imply there should be little to no difference for Treasurys with close-to-identical maturities, and so hedge funds, broker-dealers and other fast-moving traders will try to take advantage and bet that this spread, or basis, will eventually narrow.

For example, a patient trader could short an on-the-run 30-year bond maturing in 30 years and buy an off-the-run 30-year bond that was issued half a year ago. After a few months, the on-the-run bond becomes an off-the-run, losing value and eventually trading in line with the other off-the-run bonds. By doing this, the trader profits from this convergence.

Postcrisis liquidity

During times of intense volatility like this week, dealers, however, will demand a hefty premium to trade off-the-run Treasurys, as it could be difficult to take them onto their balance sheet and offload them again to a willing buyer.

“In the high-speed, high-volume, intense trading in the last few weeks, it’s hard to turn your inventory quickly around,” said Jim Vogel, an interest-rate strategist at FHN Financial.

On the other side, mutual funds and other investors promise their clients that they will be able to pull money in and out of funds on a day-to-day basis. These investors who have seen their off-the-run Treasurys holdings record double-digit gains in the span of a few weeks are now trying to sell their bonds and book profits, said market participants.

This mismatch in demand has led to a surge in the difference between the prices offered by buyers and the prices sellers are willing to accept, or the bid-ask spread, for off-the-run bonds.

“The market might clear. You just won’t like the price,” said Susan Estes, president and chief executive of OpenDoor Securities, a trading platform for off-the-run Treasurys, and a former member of the Treasury Borrowing Advisory Committee.

Investors say the lack of liquidity has also been compounded by changes in the overall bond market’s infrastructure since the financial crisis.

The consolidation of banks in the aftermath of 2008 means the bond market is now relying on a narrower group of broker-dealers to connect market participants who want to buy and sell their bonds. In addition, dealers have been saddled with post-crisis regulations that mean they cannot lever up their balance sheet to trade at a much larger capacity like they could in the past.

“Pre-crisis, on-the-runs and off-the-runs were indistinguishable as pools of liquidity,” said Estes.

Di Galoma says the bid-ask spread for an off-the-run 10-year note was as high as 50 basis points on Thursday. In other words, to sell $1 million of such notes, investors would have to give up $5,000 of the overall transaction’s value to complete the trade.

Bid-ask spreads for the 10-year note would usually stand at around a single to a few basis points.

In the context of the hundreds of billions worth of bonds changing hands every day, trading costs can thus head into the millions of dollars. For example, close to $5.7 trillion worth of Treasurys were traded in last week alone, according to the Financial Industry Regulatory Authority.

“You couldn’t trade off-the-run Treasurys even if you begged people,” said Gang Hu, managing director of WinShore Capital Management, a fixed-income hedge fund.

Faranello concurred. On Monday, there were times when traders could not find anyone willing to sell off-the-run 30-year bonds, a rare occasion in the most liquid financial asset in the world, he said.

At the end of the day, the 30-year bond yield TMUBMUSD30Y, 1.643% had booked the biggest back-to-back decline since October 1987, the month of the Black Monday stock market crash.

Funding strains?

Trading costs for off-the-run Treasurys tend to blow up when strains arise in short-term funding markets as they did when the 1998 implosion of the hedge fund Long-Term Capital Management, which had borrowed from short-term funding markets to scale up its billion-dollar wagers on bond-market spreads such as those between older and newer Treasurys to narrow.

In 1998 a lack of illiquidity amid worries over financial crises in Europe and emerging markets saw demand for the most liquid on-the-run Treasurys soar and appetite for off-the-run bonds dwindle.

This blew up the price difference between the two buckets of bonds, forcing LTCM to unwind and liquidate its positions, and freezing funding markets as banks realized one of their biggest borrowers was at the risk of collapsing.

Read: New York Fed to add liquidity into short-term markets unsettled by coronavirus

But market participants say the recent blow-out of bid-ask spreads for older Treasurys is not so much a reflection of funding pressures, and more a reflection of how dealers were struggling to handle unprecedented daily volatility in the bond-market.

It’s why Priya Misra, global head of rates strategy at TD Securities, in an interview with Bloomberg Television said the Fed’s repo liquidity injections would not help smooth dislocations in the Treasury market.

The U.S. central bank offered up $1.5 trillion of funds through longer-term repurchasing operations this week, in which it lends short-term funds to designated broker-dealers in return for collateral such sa Treasurys. The take-up of the operation was, however, limited.

Investors also point out funding costs have remained contained.

At the start of Tuesday, market participants could borrow in overnight repo markets at 10 to 15 basis points above the Federal Reserve’s benchmark interest rate, or around 1.2%, said Hu. That same session saw the biggest rally in the 10-year benchmark Treasury note since 2009.

This compared with the seizure in funding markets last September which saw overnight borrowing costs jump to as high as 10%.

Stepping in

Indeed, the Fed appears to be switching tack.

Beyond increasing the size and maturity of its repurchasing operations, the New York Fed said Thursday the $60 billion of bonds it was scheduled to buy from mid-March to mid-April would not only target short-term Treasury bills, but government bonds across all maturities.

Analysts say this tweak is targeted directly at easing the lack of liquidity in off-the-run Treasurys, as the Fed’s purchases of longer-term bonds would target older issuance not newer debt, wrote Kathy Bostjancic, chief U.S. financial economist at Oxford Economics.

And on Sunday, the U.S. central bank said it would buy at $500 billion in Treasury securities and $200 billion in mortgage-backed securities over the coming months, beginning on Monday. Investors said these purchases are likely to be aimed at the off-the-run bond market.

Treasury issuance

Investors say the lack of liquidity in the off-the-run Treasurys shines a light on the workings of financial markets, at a time when it could come under increased pressure in the coming months as the coronavirus epidemic impacts economies and markets.

As the U.S. Treasury Department ramps up bond issuance to accommodate the government’s bulging fiscal deficits, the amount of new debt issuance that cascades into the pool of older off-the-run bonds will increase with every year.

“The off-the-run market has become more and more critical, the U.S. is issuing more and more debt,” said Faranello

Se dopo avere letto questo articolo che vi riportiamo (eventualmente, tradotto con un traduttore sul Web) qualche cosa ancora vi sfugge, allora vi chiediamo di leggere anche le dichiarazioni del Chairman della Federal Reserve, Jay Powell, dopo la riunione della Federal Reserve del 10 giugno scorso, ovvero quattro mesi fa:

In its statement, the Fed said it would increase its holdings of US Treasuries and agency mortgage-backed securities “at least at the current pace to sustain smooth market functioning”. Later on Wednesday it announced plans to buy about $80bn of Treasuries between June 12 and July 13, maintaining its roughly $20bn a week rate.

During his news conference, Mr Powell pushed back against criticism that the Fed’s easy money policy had unduly lifted asset prices — particularly the share values of risky companies — and risked destabilising markets in the future and exacerbating economic inequality. “What our tools were put to work to do was to restore the markets to function, and I think some of that has really happened . . . and that’s a good thing,” Mr Powell said.

Queste frasi sono, al tempo stesso, chiare ed in forte contrasto con altre parole di Powell, che lui disse quel medesimo giorno.

“I think our principal focus is on the state of the economy, and on the labour market, and on inflation,” he added, dismissing “the concept that we would hold back because we think asset prices are too high” as detrimental to “the people that we are actually legally supposed to be serving”.

Ci sono tre cose, in queste frasi, che ogni investitore farebbe bene a tenere a mente:

la Federal Reserve è stata creata per servire gli interessi della collettività (Powell dice “del popolo”); Powell stesso dice “quel popolo che si assume che noi dovremmo servire

la Federal Reserve ha due obbiettivi definiti dal proprio Statuto: da un lato la massima crescita dell’economia, dall’altro il controllo dell’inflazione, e lo dice anche Powell

poi però Powell dice: “ci rifiutiamo di moderare gli interventi soltanto perché i prezzi degli asset finanziari sono troppo elevati”.

Frasi contradditorie fra loro, ed in contraddizione con le frasi precedenti che vi abbiamo riportato: ed in particolare con la frase che dice “ciò che ci proponevamo, mettendo al lavoro i nostri strumenti, è di mantenere in funzione i mercati finanziari”. Quindi: i mercati finanziari, oppure l’economia?

Le contraddizioni sono evidenti, ma forse qualcuno tra i lettori si sta chiedendo: “e dove sta il problema, per mé?”.

Il problema, il vostro problema, amici lettori e investitori, il vostro problema urgente, ed il vostro problema quotidiano è facile da spiegare, e noi lo facciamo con due sole frasi:

Powell giustifica le proprie azioni spiegando che aveva l’obbligo di “mantenere i mercati finanziari funzionanti”, a prima vista, e sulla base dell’intuito, è condivisibile; poi però riflettendoci viene alla mente una domanda: è vero quello che dice Powell, ovvero che “mantenere i mercati funzionanti” è un modo per “aiutare l’economia”? Chi lo dice? Che cosa lo dimostra? Chi lo ha scritto? Quali meccanismi dovrebbero mettersi in moto?

Powell afferma che non vuole “tirarsi indietro soltanto perché i prezzi sui mercati finanziari sono troppo elevati”. E qui, la cosa diventa davvero preoccupante. Per noi investitori. Perché qui Powell dimentica (e nessuno lo aiuta!) (oppure forse fa finta, di dimenticare) (ma a nessuno viene in mente di fare una domanda? é possibile?) dimentica che la più dolorosa vicenda economica degli ultimi 70 anni, che colpì noi come cittadini, come madri e padri e fratelli e figli, e che a quel tempo fu altrettanto grave del COVID-19, è quella che fu chiamata Grande Crisi Finanziaria, si svolse tra il 2007 ed il 2009, e portò vicinissimi al fallimento tutti i grandi Stati Industrializzati. E sono trascorsi appena 13 anni: come si fa, a dimenticare che la Grande Crisi Finanziaria fu provocata esattamente da quel fatto, proprio da quello che Powell ha definito il 10 giugno “asset prices are too high”?. Come è possibile dimenticare il diluvio di promesse, che fu fatto allora, quando anche la Federal Reserve ci spiegò che “ad ogni costo si eviterà il ripetersi di una situazione di questo tipo”. E oggi, invece, ci siamo di nuovo: anzi, oggi è peggio.

Non potete sfuggire a queste domande, se avete soldi investiti sui mercati finanziari: le due questioni oggi sono al centro dell’attenzione, e dei pensieri di ogni investitore che abbia ancora un minimo di raziocinio, e da ogni professionista minimamente qualificato, che abbia conservato anche un livello bassissimo di senso di responsabilità.

Rivediamo i nostri due punti precedenti, riscrivendoli con nostre parole:

è giustificato assumere che concentrando i supporti, le facilitazioni, i favori, i regali sul settore delle banche e della Borsa, si ottiene poi davvero un miglioramento dell’economia che consuma, che produce, che investe? Non esiste un solo, anche misero documento che lo prova, meno ancora un dato (leggete ad esempio nel grafico sotto). Ad oggi, si tratta unicamente di parole, di promesse. promesse di comodo? parole strumentali, per sfuggire all’imbarazzo? Lo sapremo tutti a breve, perché la cosiddetta “seconda ondata” dell’epidemia sarà esattamente il test perfetto per questo tipo di affermazioni

è giustificato dimenticare la Grande Crisi Finanziaria del 2007-2009? dimenticare che “prezzi troppo elevati degli asset finanziaria” citati da Powell possono distruggere le economie reali, come fecero tredici anni fa?

I due temi meriterebbero (e forse meriteranno) due Longform’d dedicati in esclusiva ad ognuno. Oggi, non c’è lo spazio. Possiamo soltanto testimoniarvi, con due immagini sotto, che all’interno della Federal Reserve le opinioni che Powell espresse in giugno sono, a tutto oggi, ampiamente condivise. E’ questa la nuova linea, ed è questa la nuova ortodossia che circola negli ambienti delle Banche Centrali.

Dove ci sta portando, questa gente? Noi e voi, come investitori, siamo chiamati a rispondere oggi, e non dopo, quando un eventuale danno ai portafogli titoli sarà già stato fatto. Numerosi investitori ragionano (o meglio, non ragionano) in questo modo: le Banche Centrali sono onnipotenti, e i banchieri centrali sono sovraumani. Non possono sbagliare, non hanno mai sbagliato, e vinceranno sempre sui mercati.

Recce’d la pensa nel modo opposto: i banchieri centrali sono funzionari pubblici, molto umani, esattamente come quelli che stanno al Ministero, alla Regione ed alla Provincia. Anche volendo escludere la malafede (cosa che a noi, negli ultimi anni, è risultata via via più difficile) si tratta di uomini con una loro esperienza ed un loro bagaglio. Non necessariamente, uomini infallibili, e non necessariamente uomini che hanno un grado elevato di comprensione delle economie reali. Quanto ai mercati finanziari, questi uomini che abbiamo oggi sicuramente hanno poca esperienza diretta, una conoscenza superficiale, e sono supportati sicuramente da un set di dati non completo.

E poi, c’è la storia recente: dal Duemila ad oggi, due profonde crisi finanziarie ed una terza che fino ad oggi è stata messa in frigorifero. Per essere infallibili, hanno davvero fallito un bel po’.

Oggi, poi, come detto, in questo 2020, i banchieri centrali hanno perso la loro autonomia di giudizio, sono stati costretti (dai fatti, dalle economie, ma soprattutto dalla fragilità dei mercati) a fare mosse non sperimentate prima, mai testate, del tutto azzardate, e a costruire dopo, a posteriori, una spiegazione (che è una giustificazione) per le loro scelte.

E’ stata fabbricata una teoria, a questo scopo: che dice che “non importa quanto sono elevati i prezzi degli asset finanziari: la bolla finanziaria è a fin di bene se salva i posti di lavoro” (sopra). Si tratta di un’affermazione, una speranza, si tratta di parole: neppure troppo intelligenti.

Questa speranza è destinata a fallire,. per una ragione semplicissima: perché prezzi degli asset finanziari essendo “troppo elevati” trascineranno al ribasso non solo le Borse e le obbligazioni, ma pure le economie, come avvenne nel 2000-2003, e poi nel 2007-2009.

Come abbiamo scritto già nel nostro primo Longform’d, il punto critico, il primo ambiente che mostrerà profonde crepe, è il mercato del debito (e ne stiamo parlando ogni mattina, in queste settimane, nel nostro The Morning Brief riservato ai nostri Clienti.

Negli Stati Uniti, come anche in tutto il mondo occidentale, la risposta alla crisi economica che si è manifestata fin dalla fine del 2018 (parole di Draghi e di Powell) e che poi è esplosa un anno e mezzo dopo con la pandemia COVID-19 è stata affidata alla crescita (esplosiva) dei debiti. A fronte di un PIL in netto calo, è quindi esploso anche il rapporto tra debito e PIL.

Come abbiamo già scritto, per ogni unità di debito, allo stato delle cose come è oggi, c’è quindi meno valore sella produzione. Di fatto, il valore del debito è già stato ridotto.

La scelta delle Banche Centrali (che proprio in questo senso sono le nemiche di tutti noi investitori) è stato quello di garantire a questo debito un valore del tutto artificiale, slegato dalla realtà: lo hanno fatto acquistando loro stesse i titoli, con denaro di nuova creazione, ovvero con denaro che prima non esisteva.

Potrebbero, le Banche Centrali, comperare tutto il debito del Mondo, e risolvere così la questione? Sì, potrebbero stampare la moneta necessaria per comperare tutto il debito del Mondo: ma poi, non esisterebbe più un mercato. E tutto crollerebbe in un solo istante. Il mercato può fare a meno delle Banche Centrali, ma le Banche Centrali non esisterebbero, senza un mercato.

Da qui, Recce’d ripartirà con il suo terzo Longform’d, che per il momento sarà ancora gratuito e leggibile in questo Blog.