Noi di Recce’d non ci occuperemo quindi di ciò che accade in Italia, bensì delle tendenze internazionali: tendenze da cui dipende anche la fine che faranno questi esperimenti italiani. Prenderemo spunto, per il nostro lavoro, dai temi trattati in questo articolo del Financial Times dello scorso mese di gennaio: a noi interessa di aiutare i Clienti, ed i potenziali Clienti, a capire, e NON a vendere. Recce’d non ha “prodotti finanziari” da vendervi, non Fondi Comuni, non GPM, non GPF, e nessun altro intruglio del genere. Il nostro Post prosegue più in basso. dopo l’articolo del Financial Times, articolo che vi sarà di grande aiuto per capire come stanno davvero di cose.

JANUARY 17 2020 51

Quantitative, automated strategies have long appeared to be the new, exciting frontier for investing, but many are suffering a rough patch — raising questions about an industry that has enjoyed huge inflows over the past decade. Just 15 per cent of quant mutual funds beat the US stock market last year, according to Nomura: a performance that trailed even behind traditional stockpicking funds, which suffered their own poor run.

Explanations for the disappointing results vary, from popularity eroding quant strategies’ effectiveness to the impact of seesawing bond yields on certain market signals, but some analysts say this is more than a blip. The industry is going through a “quant winter”, argues Joseph Mezrich, head of quantitative strategies at Nomura Instinet. The performance has been “pretty terrible” for two years now, he points out.

Clifford Asness, the head of AQR Capital Management, said: “This is indeed a quant winter, but two-year winters just happen. We don’t know how to predict them, or when they end, but we know they occur.” Quantitative investing is a broad term.

Quant mutual funds mostly harness bigger, well-known “factors”, such as the tendency for companies with stable earnings growth or strong momentum to do well. There is roughly $160bn of assets in these stocks-focused quant mutual funds, according to Nomura.

Quant hedge funds are also a diverse crowd, but they tend to scour markets for fainter, rapid signals, and are usually staffed by scientists and programmers rather than people with a background in economics or finance. They trade a wider array of assets than just stocks, and go both long and short — in other words, they try to make money from securities both falling and rising. Their performance has also been a mixed bag. Bridgewater’s Pure Alpha fund was flat for 2019. Renaissance’s Institutional Equities fund gained 14.2 per cent, while its institutional Diversified Alpha fund returned 4.7 per cent. DE Shaw’s flagship Composite fund made 10.9 per cent, while its equities-focused fund Valence eked out a 5.5 per cent gain.

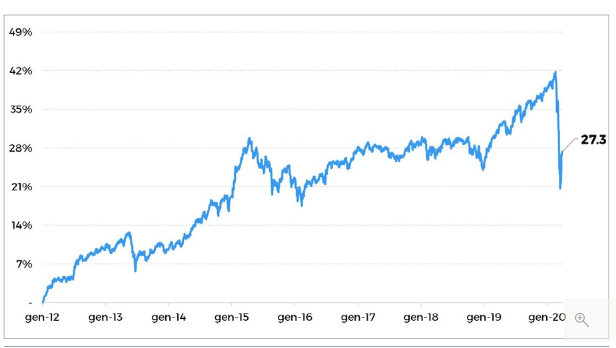

Some firms are trimming their headcount. The founder of hedge fund WorldQuant, former computer games programmer Igor Tulchinsky, once predicted that a “Quantasaurus” would trample over traditional investing. But WorldQuant is reportedly cutting 130 jobs and shutting five international offices. The firm declined to comment. AQR, one of the biggest managers of quant mutual funds, has also announced another round of job cuts, after its assets under management fell by almost a fifth over the past couple of years to $186bn.

The industry’s performance has hardly been disastrous. Quant mutual funds returned on average 27.7 per cent in 2019, according to Bank of America, and quant equity hedge funds returned 11.8 per cent, according to HFR. This is worse than the broader stock market, but still represents a decent year in nominal if not relative terms. The question is whether this is simply an uncomfortably-long but temporary poor spell, or if there is something broader at work. Mr Asness argues that the pain of poor periods is precisely why many factors continue to work in the longer run, despite being well known. “When [quant winters] occur everyone goes into overtime trying to explain why winter came. But it just does happen,” he said. “Of course, this is like saying ‘there will be a bear stock market again’. It’s absolutely true, but if you can’t predict when, you stay invested and earn the long-term return.”

Others are not so sure. Yin Luo, head of quantitative strategy at Wolfe Research, agrees that there is a degree of cyclicality to quant factors, but argues that their popularity is eroding the above-market returns — the “alpha”, in Wall Street jargon — that they have historically produced. “These strategies are becoming better and better known, so the alpha is disappearing,” he said. “This does feel like another quant winter . . . The crowding will come down and the returns will come back, but the longer-term trend is that most of it is going away.” Mr Mezrich is sceptical that crowding explains why quant funds have fizzled. He thinks it is better explained by how tumbling bond yields have warped market dynamics, making previously disparate factors more correlated, and how quant funds can get hit when they reshuffle their positions. “It’s mainly because macro isn’t part of their risk management repertoire,” he said. This might mean the current fallow period does not last. But it could more likely mean that many quant strategies are in for a long rocky ride, Mr Mezrich argues. “They may come back, but you have to be very certain about the macro environment,” he warned. “If Japanification [permanently low interest rates] grips the world then this could be with us for a long time.”

Nel frattempo, su questo medesimo tema noi di Recce’d stiamo producendo da mesi un contributo settimanale a Soldionline.it, contributo che nelle prossime settimane arriverà proprio ad occuparsi di ROBO ADVISORS, di Finanza Quantitativa, di modelli e di fattori.

Chiudiamo il Post con un suggerimento: amici lettori, fate attenzione, e non fatevi ingannare da “ricette miracolose.”.

Da tredici anni, Recce’d vi ripete: la Finanza Quantitativa è una cosa seria, e va utilizzata in modo serio, e non è un giocattolo per bambini. Wealth managers, private bankers, family bankers, personal bankers, “consulenti abilitati alla vendita fuori sede” ovvero i promotori finanziari e consulenti online, neppure sanno che cosa sia, un algoritmo, ed usano il termine “algoritmo” in modo pretestuoso, come uno slogan commerciale, senza capirne il senso.

Recce’d utilizza l’analisi quantitativa, ed anche quei “mille miliardi di dati” di cui in tanti si vantano, nel modo opposto. Non si fa guidare, ma ne guida l’utilizzo. Non affida i soldi dei Clienti alla macchina: siamo noi a usare la macchina, nell’interesse esclusivo del Cliente. Noi sappiamo come si fa.

Recce’d infatti è consapevole dei limiti di questi strumenti: perché se ne occupa dagli Anni Ottanta, direttamente, e come gestore di portafoglio (mai operato come venditore, chi lavora in Recce’d).

In Recce’d utilizziamo il QUANT, ma non ci facciamo usare dal Quanti: lo utilizziamo, ma in modo consapevole. E solo per fare l’interesse del Cliente,. mai per vendere “prodotti finanziari” come GPM, GPF, e attraverso queste i soliti Fondi Comuni di Investimento (magari nascondendo le retrocessioni che ricevono dai Fondi Comuni sotto forma di commissioni “soft”, e poi dire che “non si ricevono retrocessioni”: un trucco vecchissimo)..

Intanto che noi lavoriamo, restiamo sempre in attesa di ascoltare il parere di CONSOB ed OCF su questo tema (e perché no, magari anche su BARRA, sempre ammesso che sappiano di che cosa stiamo parlando).