Ovviamente, il titolo di questo nostro Post è ironico: “non dire gatto finché non è nel sacco”, ripeteva un grande uomo di sport italiano. E al momento il sacco non si è ancora chiuso.

(Tutti i gatti ci corrono dentro, però.)

Tuttavia: c’è almeno un punto di vista, rispetto al quale noi di Recce’d abbiamo già vinto. le cose, sono andate proprio come noi avevamo previsto, per voi e per i Clienti, più di un anno fa.

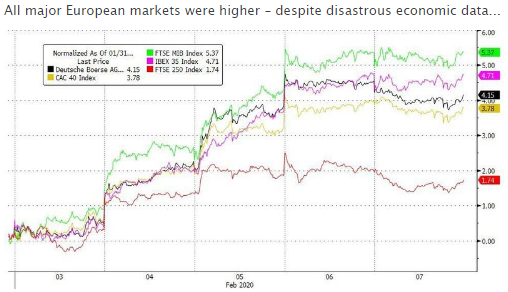

Come successe già nel 2018, e lo ricorderete sicuramente, il mercato da mesi è partito all’inseguimento di un “miraggio”. I dati dell’ultima settimana, per l’Europa e per gli Stati Uniti, ce lo hanno confermato, e per i lettori che se li sono persi ecco qui due resoconti da Reuters. Non vi serve un economista, per comprendere il significato di dati come questi per i vostri portafogli e i vostri soldi.

U.S. January core retail sales unchanged; December revised down

Lucia Mutikani· ·

WASHINGTON (Reuters) - U.S. consumer spending appears to have slowed further in January, with sales at clothing stores declining by the most since 2009, which could raise concerns about the economy’s ability to continue expanding at a moderate pace.

The mixed retail sales report from the Commerce Department on Friday also showed purchases by households were not as strong as initially reported in December.

Retail sales excluding automobiles, gasoline, building materials and food services were unchanged last month. Data for December was revised down to show the so-called core retail sales rising 0.2% instead of jumping 0.5% as previously reported. Core retail sales correspond most closely with the consumer spending component of gross domestic product.

Consumer spending accounts for more than two-thirds of U.S. economic activity. Economists polled by Reuters had forecast core retail sales rising 0.3% last month. The unchanged reading in core retail sales suggested consumer spending lost further momentum early in the first quarter after losing considerable speed in the October to December quarter.

The economy grew 2.3% in 2019, slowing from 2.9% in 2018.

With business investment continuing to falter and manufacturing depressed, consumer spending had helped to keep the longest economic expansion on record, now in its 11th year, on track.

Despite signs of continued slowdown, consumer spending remains supported by a strong labor market, which is steadily lifting wages.

U.S. stocks index future pared gains after the data. The dollar was little changed and U.S. Treasury prices were steady.

In January, overall retail sales rose 0.3%, but data for December was revised down to show sales gaining 0.2% instead of climbing 0.3% as previously reported.

Sales were lifted by a auto purchases, which rebounded 0.2% after slumping 1.7% in December. Receipts at service stations fell 0.5%. Sales at electronics and appliance stores decreased 0.5%. Sales at building material stores jumped 2.1%, the most since last August, after rising 1.3% in December. Sales were likely boosted by unseasonably mild weather, which has boosted activity in the construction sector.

Receipts at clothing stores dropped 3.1% last month, the most since March 2009. Clothing retailers have been struggling with plummeting mall traffic as consumers opt for online shopping. Macy’s announced this month plans to close 125 of its least productive stores over the next three years and cut more than 2,000 corporate jobs.

Online and mail-order retail sales rose 0.3%. That followed a 0.1% dip in December. Receipts at furniture stores rose 0.6%. Sales at restaurants and bars increased 1.2%. Spending at hobby, musical instrument and book stores edged up 0.1%.

Europe on the brink of recession

BRUSSELS (Reuters) - Euro zone economic growth slowed as expected in the last three months of 2019 as gross domestic product shrank in France and Italy against the previous quarter, but employment growth picked up more than expected, official estimates showed on Friday.

The European Union’s statistics office Eurostat said GDP in the 19 countries sharing the euro expanded 0.1% quarter-on-quarter in the October-December period, as announced on Jan 31, for a 0.9% year-on-year gain - a downward revision from the previously estimated 1.0% growth.

The quarterly growth rate slowed compared to the 0.3% expansion in the third quarter because of a 0.1% contraction in the second biggest economy France and a 0.3% contraction in the third biggest Italy.

Growth Germany, the biggest euro zone economy, stagnated.

Eurostat also said that euro zone employment rose 0.3% quarter-on-quarter in the last three months of 2019 for a 1.0% year-on-year gain. Economists polled by Reuters had expected a 0.1% quarterly rise and a 0.8% annual increase.

Separately, Eurostat said the euro zone’s trade surplus with the rest of the world was 23.1 billion euros in December, up from 16.3 billion a year earlier, bringing the total for the whole of 2019 to 225.7 billion, up from 194.6 billion in 2018.

Adjusted for seasonal factors, the trade surplus was 22.2 billion in December, up from 19.1 billion in November as exports rose 0.9% on the month and imports fell 0.7%.

Allora, nel gennaio 2018, il miraggio si chiamava “crescita globale sincronizzata”. Qualche cosa a cui la maggior parte di voi ai tempi credeva. Peccato che non è mai esistita. Mai, non ci siamo andati neppure vicino. Un miraggio, hanno detto poi a fine anno gli strategisti e i commentatori. Un abbaglio collettivo. Un abbaglio collettivo non casuale e manovrato

Oggi, la situazione è la medesima del gennaio 2018. La reflazione, la stabilizzazione, la ripresa: quante volte ve la hanno venduta, nel 2019, e quante volte avete dato fiducia a quei soggetti che ve la vendevano, come se fosse un divano venduto alla tv che ha un “valore commerciale di 500 euro” ma che voi potreste acquistare per 100 euro?

Nel pubblico dei risparmiatori sono in molti a cui piace andare avanti così. A molti piace essere imboniti: che poi vuol dire farsi portare a spasso da un imbonitore, un sorridente soggetto vestito in modo eccessivamente formale che vi vuole sempre, e comunque “tranquillizzare, anestetizzare, isolare dal Mondo”, il Mondo quello vero. A lui, voi pagate senza saperlo il 3,5% ogni anno, sia che le vostre cose vadano bene sia che invece vadano male.

Miracolati, questi imbonitori: il 2019 ha salvato a loro il lavoro, e la carriera. L’anno era iniziato con la Borsa di New York in un bear market (-20%) che avrebbe tranquillamente potuto continuare. Invece, alla fine del 2019 il medesimo indice aveva messo insieme il più ampio rialzo degli ultimi 10 anni.

E tutti voi lettori di Recce’d sapete benissimo che cosa c’è dietro al rialzo.

In particolare, da settembre in avanti, c’è questa favola della “stabilizzazione, reflazione, ripresa graduale”: che appunto non esiste.

Visto che non siamo più nell’età (dorata) dell’adolescenza, noi non crediamo più alle favole, e neppure ai supereroi invincibili: ma la massa, loro, si sono fatti convincere che gli errori invincibili esistono, che non spaglieranno mai, che si andrà avanti così per sempre, e che per sempre le Borse resteranno sui massimi.

(Anche perché, ovviamente, nel 2008 la Federal Reserve non esisteva ancora, no?).

A tutti questi investitori, che amano credere ai supereroi (perché rassicurano chi è insicuro di ciò che pensa) oggi Recce’d vuole ricordare che ogni film con i supereroi dopo due ore finisce, e quando si esce dal cinema, poi per strada non trovate Superman, ma al massimo l’automezzo che porta via la spazzatura.

Salvo che poi non lo si voglia vedere anche se non esiste, Superman.