Oggi Recce’d pubblica sette nuovi Post. Il lancio della nuova impostazione di questo Blog (a temi, e con un nuovo layout) è stato rinviato al secondo trimestre 2021 in ragione della rapidissima evoluzione della situazione dei mercati finanziari nel mese di gennaio. Per noi di Recce’d, sono sempre i mercati a dettare i tempi. In aggiunta, oggi le occasioni per gli investitori sono le più grandi di una generazione. e noi di certo non vogliamo perderle di vista.

Mentre Mario Draghi crea un Ministero della Transizione Verde (noi il verde Lega ma il verde ambientalista) e mentre Joe Biden dedica una parte importante del suo Piano da 2000 miliardi (forse solo 1400 miliardi?) che dovrebbe essere varato nel mese di marzo (dovrebbe), anche sui mercati finanziari circola con grandissima insistenza la parola “surriscaldamento”. ma non si tratta del problema ambientale.

Il “surriscaldamento” del quale si discute ogni giorno sui mercati di tutto il mondo è un fenomeno duplice:

da un lato c’è il surriscaldamento dei prezzi, alla produzione ed al consumo,

e dall’altro c’è il surriscaldamento dei prezzi sui mercati finanziari

Anche se il dato per l’inflazione che è stato pubblicato lo scorso mercoledì negli Stati Uniti è risultato inferiore a ciò che veniva previsto dagli economisti, resta il fatto che tra gli operatori si discute, con frequenza, di una possibile inflazione al 4% per gli Stati uniti, dal mese di agosto in avanti.

Con la sua ben nota maestria, Mohamed El Erian ha preso spunto proprio da questo, per scrivere un articolo (sul Financial Times) che unisce la sua analisi del tema inflazione alla sua analisi del tema “surriscaldamento dei mercati”.

In questa occasione, la nostra sintonia con ciò che El Erian scrive è vicina al 100%. “Mind the gap”, ci spiega El Erian: che in italiano si può tradurre “Fate attenzione al buco”. Ed in effetti, per tutti noi investitori, il rischio è quello di “cadere nella voragine”: e si può essere certi che un buon numero di investitori ci cascherà dentro, e con tutti e due i piedi.

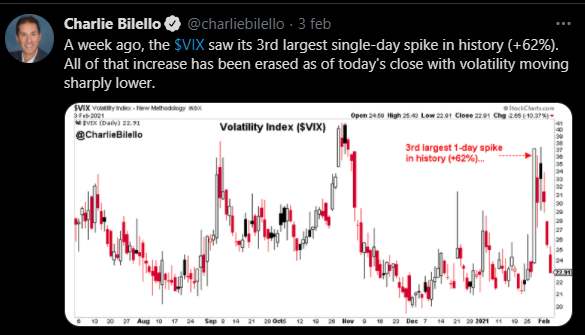

Questo perché il “surriscaldamento” oggi è un problema che investe anche gli investitori: come scrive nel grafico di apertura del nostro Post il Wall Street Journal: “bloccati in casa sul divano e con nulla da fare” si perde il senso della realtà, e accadono le cose che si vedono poi sotto, nei due grafici.

Da questa situazione deriveranno le inevitabili turbolenze, e molti investitori si renderanno conto di avere tenuto troppo rischio in portafoglio, nonostante i mille segnali ed avvertimenti, forniti anche da noi.

Ciò che Recce’d può fare per voi, dopo che avrete letto questo articolo, è operare in modo tale da garantire al Cliente sia un rendimento decente (anche se i mercati in un dato momento ci vanno contro) sia un controllo del rischio stretto, e di elevato livello qualitativo.

Leggiamo quindi insieme le parole di El Erian: se poi volete anche sapere che cosa fare, non avete che da contattarci.

The economic and financial data so far this week have highlighted once again the enormous contrast between the reported inflation rate for goods and services and the one for asset prices. It is part of a much bigger and consequential disconnect between the economy and financial markets, or what is commonly referred to as Main Street versus Wall Street. In the short term, it opens a bigger window for significant additional fiscal stimulus to supplement ultra-loose monetary policy and financial conditions. But it does so at the risk of amplifying the policy, financial stability and political risks that await us down the road.

For the second consecutive month, the core consumer price index, which excludes volatile food and energy costs, was flat for January; the core annual inflation rate was 1.4%, down from 1.6% in December. Both outcomes were below analysts’ median forecast of a gain of 0.2% month over month and 1.5% year over year. The overall inflation rate rose 0.3% from the previous month and 1.4% from a year earlier.

The muted inflationary data come at an important time for a Biden administration seeking backing for a sweeping fiscal package. Congress is now considering the first of two components, focused on providing $1.9 trillion in immediate relief for multiple segments of the population and in countering Covid-19 by controlling the infection rate and speeding up vaccinations. Consensus expectations for what is likely to emerge from the inevitably noisy legislative process are now in the range of $1.5 trillion to $1.6 trillion, with as much as $2 trillion penciled in by some for the second multiyear recovery-focused component.

When combined with the continued exceptional liquidity injection of $120 billion a month signaled by the Federal Reserve, the U.S. economy is looking at an additional 15% to 25% of gross domestic product in stimulus this year alone, coming on top of what was even more for 2020. No wonder both stock and bond prices jumped immediately after the release of the muted inflation data. In doing so, they amplified what is already an enormous gap between a sluggish economy in terms of both growth and inflation and buoyant finance.

Fresh records for U.S. stock indexes are not — by far — the only sign of booming Wall Street conditions. January was yet another strong month for a wide range of contributors to the financial sector’s bottom line, including price increases for the vast majority of risk assets, massive additional fund inflows, heightened SPAC activity and greater corporate bond issuance. This comes on top of an incredibly remunerative 2020, which produced booming profits and, according to the latest Bloomberg estimates, some $23 billion of compensation for the top 15 earning hedge fund managers.

But what is favorable for policy and markets now increases future risks, starting with financial instability. The more Wall Street surges ahead in the short term, the harder it is for eventually improving economic conditions to validate the ever more elevated asset prices in an orderly manner. This makes it more difficult to carry out the needed policy transition in which massive fiscal stimulus allows for a moderation of what has been exceptionally loose monetary stimulus. It also makes the much needed catch-up of nonbank sector regulation and supervision harder to undertake smoothly. All this is in the context not just of the enormous disconnect between Main Street and Wall Street, which is attracting greater social and political attention, but also of the warning signals from the Robinhood-Reddit-GameStop frenzy.

The big hope — for policy makers, markets, the economy and, most importantly, society as a whole — is that faster growth that is also more inclusive and sustainable will validate elevated asset prices, facilitate the policy transition and avoid the type of financial dislocations that undermine economic well-being. The risk is twofold: that the muted inflation data prove to be a head fake rather than an indication of the future and that the challenge of eventually closing the economy-finance gap is made even more difficult by an additional liquidity-driven short-term sprint in markets.