Ya gotta believe

Ciò che qualifica il lavoro di un gestore del portafoglio è la capacità di prospettare ai propri Clienti, nel modo più corretto possibile, gli scenari che il suo portafoglio di investimenti dovrà affrontare.

Questo è il metro sul quale noi, in Recce’d, ci misuriamo ogni mattina. Quello che accade nella realtà del Mondo (produzione, lavoro, inflazione, ed anche politica, relazioni internazionali, guerre) corrisponde a ciò che noi avevamo anticipato ai nostri Clienti?

Facciamo, insieme ai lettori del Blog, un test in tempo reale. Attraverso il nostro sito, noi di Recce’d vi avevamo detto:

che il 2021 non avrebbe avuto nulla in comune con il 2020, ed è già così oggi: lo avete visto tutti

che il 2021 sarebbe risultato un anno molto diverso da quello raccontato a fine 2020 dalle banche globali di investimento e dalle Reti di promotori: e nel solo mese di gennaio avete ricevuto due-tre conferme

che il 2021 avrebbe portato una serie di eventi e fatti non immaginabili solo pochi mesi prima: dal Campidoglio a Gamestop, le conferme non sono mancate

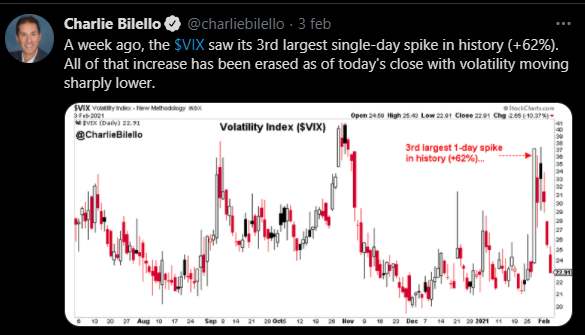

che la fragilità dei mercati finanziari deriva soprattutto … dai mercati finanziari medesimi, e solo otto giorni fa era questo il tema che dominava le nostre e le vostre giornate

che il COVID-19 ed “il vaccino” non sono notizie rilevanti per i mercati finanziari, ed infatti in questa prima settimana di febbraio quando si parla di mercati ed investimenti del vaccino non ti parla più nessuno

Per i vostri investimenti, a questo punto, potrebbe risultare utile andare a cercare quelle cose che Recce’d ha anticipato nel 2021 e che devono ancora verificarsi. Quelle che non avete ancora letto in prima pagina sul Sole 24 Ore oppure degli altri quotidiani. Perché potrebbe essere quella, la prossima cosa che i vostri investimento devono affrontare.

Ragione per la quale, potrebbe essere un buon investimento di tempo quello di ritornare indietro, e rileggere nel Blog tutte le nostre analisi degli ultimi 12 mesi.

Come sempre, Recce’d non si limita a proporre le proprie analisi e le proprie tesi, quelle che fanno da supporto fondamentale alla propria strategia di investimento. Senza timore e senza giri di parole, Recce’d vi mette a disposizione anche le idee e le indicazioni degli altri.

In questo Post, ad esempio, facciamo il punto al 6 febbraio 2021 utilizzando le parole degli altri.

Tornando a ciò che si diceva prima, queste sono le cose che Recce’d ha detto che NON si verificheranno. Lo scriviamo qui ed oggi, poi torneremo a leggerlo tra qualche settimana e mese.

Il titolo che leggete nell’immagine ci dice che: “la tesi della reflazione si sta rafforzando, ed è per questo che le azioni (americane) mettono a segno nuovi record.

E’ vero? Non è vero? E’ un riflesso delle isterie assortite di questo mercato, del mercato di Gamestop?

Amici lettori, questo lo dovete decidere da soli, e nel vostro migliore interesse: noi, per la nostra parte, abbiamo già preso le decisioni migliori.

Nel brevissimo testo che segue, scritto oggi sabato 6 febbraio, si riassumono tutti i punti forti della “tesi reflazione”. C’è tutto in poche righe: il piano di Biden, lo stimolo alla crescita dell’economia, le prospettive di un ulteriore rialzo della Borsa, il rialzo dei rendimenti delle obbligazioni. Leggete e poi chiedetevi: mi convince?

“We believe that we are still in the early stages of a new bull market, transitioning from the 'hope' phase (which typically starts during a recession, led by rising valuations) to a longer 'growth' phase as strong profit growth emerges,” chief global equity strategist Peter Oppenheimer wrote in a 4 February client note.

Yet the fundamentally more important financial development was, as usual, in the bond market. The yield curve—the graph of Treasuries from short- to long-term maturities—is the most sharply upwardly sloped in years. That’s a result of longer-term yields climbing, with the benchmark 10-year note ending the week at 1.17%, near the high end of its recent trading range, and the 30-year bond at 1.98%, nearing 2% for the first time in about a year.

This is a classic indication that the bond market is anticipating stronger economic growth and higher inflation. Those expectations got a boost Friday after both houses of Congress voted to begin the process of approving President Joe Biden’s $1.9 trillion fiscal relief plan without votes from congressional Republicans.

Friday’s employment report was disappointing, however, with a smaller-than-expected 49,000 increase in nonfarm payrolls in January, and December’s job loss revised to 227,000 from the 140,000 originally reported. The unemployment rate fell to 6.3% last month from 6.7%, but mainly because of lower labor-force participation. The uninspiring data could bolster the argument for fiscal action.

The prospect of stimulus has some economists boosting growth estimates, with Nancy Lazar of Cornerstone Macro now looking for the economy to be expanding at a 7% pace by the fourth quarter, up from her previous estimate of 6%. That’s what both the bond and stock markets seem to be pricing in, which means that any shortfall in a recovery would be a surprise. So far, 2021 has been full of them.

Il secondo titolo che vi presentiamo, nell’immagine sotto, si pone una domanda: il rialzo dei rendimenti delle obbligazioni, nel 2021, ci segnala che l’inflazione sta arrivando?

Noi aggiungiamo una seconda domanda: se l’inflazione sta arrivando, e se questo aumento dell’inflazione farà aumentare anche i rendimenti obbligazionari, lo scenario di “reflazione” descritto dal brano che avete letto più in alto reggerebbe?

Secondo Goldman Sachs, la risposta è positiva.

Alla fine, ciò che si chiede all’investitore finale, è di credere. E’ di crederci. “Ya gotta believe” come diceva il famoso allenatore dei New York Mets (Tug Mc Graw) prima di ogni partita.

Qualcosa del genere anima anche i piccoli investitori negli ultimi mesi: “se ci crediamo tutti insieme, allora il titolo salirà”. Nel caso di Gamestop ha funzionato.

Come detto, noi in questo Post siamo qui a ricostruire un’atmosfera e a riportare le idee degli altri, le idee che ad oggi risultano prevalenti, guardando ai prezzi sui mercati finanziari.

Siamo però qui anche per ricordare a tutti i lettori che il gioco dei mercati finanziari in realtà NON è un gioco, ma è strettamente intrecciato con la realtà.

Ed anche che NON è semplice: è molto complesso.

Ve ne potete rendere conto facilmente, anche se leggete (ma con attenzione ed in modo critico) le parole di chi NON la vede come la vede Recce’d.

Un esempio lo trovate qui di seguito, in un articolo del quale, dopo e più in basso, noi mettiamo in evidenza quello che a nostro giudizio è il passaggio più utile per chi deve fare scelte per il futuro dei propri soldi.

Ya gotta believe, reliever Tug McGraw said of his 1973 New York Mets before they went on to win an unlikely National League pennant. Investors seemed to have embraced the same sentiment for this stock market, which continues to put every setback behind it as it marches to record highs.

The Dow Jones Industrial Average advanced 1,165.62 points, or 3.89%, to 31,148.24 this past week, while the S&P 500 rose 4.6%, to 3886.83, and the Nasdaq Composite gained 6%, to 13,856.30. The Russell 2000 left them all behind with a 7.7% jump, to 2233.33.

It was a striking turnaround following the previous week’s 3%-plus declines—and a fast one. At the end of Friday a week ago, we were concerned that the derisking—market jargon for selling—that hedge funds had to do following the GameStop (ticker: GME) short squeeze would last awhile. Instead, it appears that the pros had derisked so much during the last week of January—Fundstrat’s Tom Lee called it the “largest [hedge-fund] degrossing in a decade, second only to March 2020”—that they had to reload this past week.

They certainly had reason to. Let’s start with the economic data. While January’s payroll report was a disappointment—the U.S. added just 49,000 jobs, and December’s losses were revised even lower—everything else came up roses. The Institute for Supply Management’s services survey not only topped expectations, but the new-order and hiring components pointed to further growth ahead, and durable-goods orders topped expectations as well. The economy should also get a lift from more stimulus payments, whether through a bipartisan agreement or the Democrats passing a $1.9 trillion relief package on their own.

But the real driving force has been improving Covid-19 news. The weekly number of new cases has dropped 30% from two weeks ago. New vaccines will be on the scene soon, with Johnson & Johnson (JNJ) filing for emergency-use authorization and Novavax (NVAX) heading in that direction. At this pace, reopening should happen on schedule, letting people who work at restaurants, hotels, and elsewhere get back to work.

“The market is projecting that we see the economy pulling out of the worst of the pandemic in the second half of the year,” says Quincy Krosby, chief market strategist at Prudential Financial.

Is it ever. The Energy Select Sector SPDR exchange-traded fund (XLE) gained 8.2% this past week as oil prices climbed 8.9% to $$56.85 a barrel, the highest since January 2020. The Financial Select Sector SPDR ETF (XLF) got a boost as the 10-year Treasury yield climbed to its highest level since March. Both are signs of coming growth. On the flip side, Clorox (CLX), one of Covid’s biggest beneficiaries, tumbled 8% despite reporting better-than-expected earnings and offering above-consensus guidance. No one, it seems, wants to own a stock so closely connected to the lockdown narrative.

Wall Street is starting to believe in the reopening, too. Macquarie’s trading desk now expects the U.S. economy to grow by 7.1% in 2021, including inflation, up from its previous 4.7% estimate. It would be the strongest growth since 1983. Analysts, who have been only too happy to leave forecasts unchanged despite earnings beats, have started to change their tune, increasing their S&P 500 earnings estimates for 2021 by 2.6% this earnings season, according to Barclays strategist Maneesh Deshpande. “Analysts might be playing catch-up with their revisions as companies update their 2021 outlooks,” he explains.

Yet investors might want to listen to the bond market. The yield curve, as the difference between short- and long-term bonds is known, has been steepening rapidly, rising above one percentage point last week in the two-year/10-year curve. In the short term, that’s simply a reflection of stronger growth expectations and more inflation, and something the Federal Reserve governors are almost certainly happy to see.

But everything has its limits, and as the spread between the two bond yields nears 1.3 percentage point, it could become a problem for the stock market, explains Sevens Report’s Tom Essaye. “Historically, [a steepening yield curve is a] good sign for both the economy and stock markets in the coming months and quarters,” he writes. “But it is also an early warning sign that the clock is ticking on how long the Fed will remain on hold, or easy, before beginning to hike rates and tighten financial conditions to combat the threat of runaway inflation.”

The Fed, of course, has done its best to convince the market that it won’t start raising interest rates until 2023, no matter what markets do. How much more stocks can gain could depend on whom investors believe.

Nell’articolo che avete appena letto, trovate un aggiornatissima descrizione della “narrativa della reflazione”. E dovete crederci.

Oppure NON crederci: siete liberi di farlo, e l’alternativa è a vostra disposizione, qui in Recce’d.

Ciò che dovrebbe aiutarvi, a decidere se crederci oppure non crederci, è il passaggio che Recce’d ha evidenziato nell’articolo, insieme con il testo che accompagna il grafico più in alto, ed anche i due grafici che qui sotto fanno da chiusura al nostro Post.

E poi chiedetevi: “ma io ci credo, a questa storia?”.

I dati di questo Post vi aiuteranno. Ed anche utilizzare la vostra stessa memoria, vi aiuterà: la memoria di ciò che successe, alle economie ed anche ai vostri portafogli, sia nel 2019, sia nel 2018, sia nel 2017, sia nel 2016, sia nel 2015, e poi … continuate voi.