Longform'd. Giugno 2022: la crisi di fiducia è arrivata

Ve ne abbiamo scritto per due anni, ed ora tutti avete davanti agli occhi lo scenario che Recce’d aveva anticipato. Chi ci segue con regolarità, e trae indicazioni operative dalle nostre osservazioni, sicuramente ne sta beneficiando.

E chi ce lo dice? Niente di meno che il Governatore della Banca del Giappone, Kuroda, e nel modo più chiaro possibile. Lo vedete nelle prime tre immagini del Post, che risalgono addirittura allo scorso aprile, ma che risultano attualissime dato ciò che abbiamo saputo della riunione della Banca del Giappone di ieri 17 giugno 2022 (della riunione nello specifico scriviamo più in basso in questo Longform’d).

Negli ultimi due mesi e mezzo, il mercato ha spinto Kuroda, e la sua Banca del Giappone, ad un limite. Lo ha testato. Fino al punto che lui già nel mese di aprile era stato costretto ad uscire allo scoperto (cosa molto difficile per un giapponese) e dire “non credo che il mercato abbia perso fiducia nello yen”.

Ma soprattutto (lo leggete nella immagine che segue) Kuroda era stato costretto a dichiarare già due mesi e mezzo fa: “comperiamo Titoli di Stato solo perché vogliamo raggiungere gli obbiettivi di politica monetaria: non è vero che comperiamo i Titoli di Stato per finanziare le spasa pubblica”. Per poi concludere: “se si perde la fiducia nella capacità di controllare la spesa pubblica, poi si perde il controllo dei tassi di interesse”.

Amici lettori, che più chiaro di così non è possibile parlare. Più chiaro di così, non è possibile spiegarvi le cose. E un discorso del tutto simile andrebbe fatto, ad esempio, a proposito dei BTp italiani.

Oggi noi riprendiamo un tema che avevamo già trattato nel nostro Blog, ovvero il tema della fiducia, perché risulta sempre più evidente, anche per i meno attenti ed i meno competenti, che tutti nell’attuale scenario dei mercati gioca un ruolo importantissimo la fiducia nelle istituzioni e la credibilità delle Banche centrali e dei Governi.

Tutti i vari temi di mercato di cui leggete ogni mattina sui quotidiani (dall’inflazione alla recessione, dalle materie prime all’occupazione) si stanno riordinando come satelliti di un solo tema: il pubblico, degli investitori ma pure dei non-investitori, sta perdendo i suoi ancoraggi, i suoi punti di riferimento, ovvero sta perdendo la fiducia. Piano piano (fino ad oggi) la paura ha sostituito la fiducia.

Noi di Recce’d vi diciamo da mesi che sarà questo il principale tema di mercato 2022 - 2025.

Come già specificato, le frasi di Kuroda che leggete qui sopra risalgono al 2 aprile 2022 : e sembrano quasi profetiche. Diceva allora Kuroda: se si perde la fiducia nella politica fiscale (nel debito dello Stato), si perde il controllo dei tassi di interesse. E non soltanto di quelli, aggiunge oggi Recce’d.

Le frasi di Kuroda diventano quindi molto significative rilette oggi, a due mesi di distanza, visto ciò che è successo nel frattempo in Giappone, fino alla riunione di ieri mattina della Banca del Giappone (riunione che commentiamo più in basso in questo Longform’d). E anche vista la volatilità elevata nel comparto dei Titoli di Stato in Eurozona nel mese in corso.

Vi suggeriamo di mettere a confronto la frase di Kuroda (quella dell’immagine) con il clima che si respirava sui mercati finanziari sei mesi fa, a inizio 2022.

Vi suggeriamo in particolare di metterle a confronto con quello che per due anni il vostro wealth manager, il vostro private banker, il vostro robo advisor vi ha ripetuto.

Che cosa vi ripeteva, con tono sicuro, fino a tre-sei mesi fa? Che non c’erano rischi, per i vostri soldi, nei mercati finanziari del dopo-pandemia, perché “le Banche Centrali ci coprono le spalle”, perché “le Banche Centrali stampano moneta e quindi sono onnipotenti”, perché “le Banche Centrali hanno il controllo totale dei mercati finanziari”.

Tutte e tre, questa affermazioni, erano delle barzellette: come i fatti poi ci hanno mostrato.

E naturalmente, c’è chi ha riso molto.

Rilette oggi, a soli tre-sei mesi di distanza, quelle affermazioni, e tutti i suggerimenti e i consigli operativi che ne derivavano (“è questo il momento di investire in Borsa”, “i mercati recuperano sempre”, “è assurdo oggi stare fuori dalla Borsa”) fanno sorridere.

E una bella risata, dicono, allunga la vita.

Purtroppo però non è con una risata che si risolvono i dubbi sui propri investimenti e sul proprio portafoglio in titoli. Per fare le scelte giuste, ci vuole altro.

Ci vuole in primo luogo la capacità di analizzare, in modo analitico ed anche critico, la situazione attuale (dei mercati, delle economie, delle società), unita alla capacità di ricavarne poi indicazioni utili alla stima di rendimenti e rischi sui mercati finanziari di qui a tre, sei, dodici mesi. Ed arrivare in questo modo a fare le giuste scelte per il proprio portafoglio in titoli.

Chi potrebbe aiutarci, in questo difficile compito?

Forse la Banca Centrale Europea?

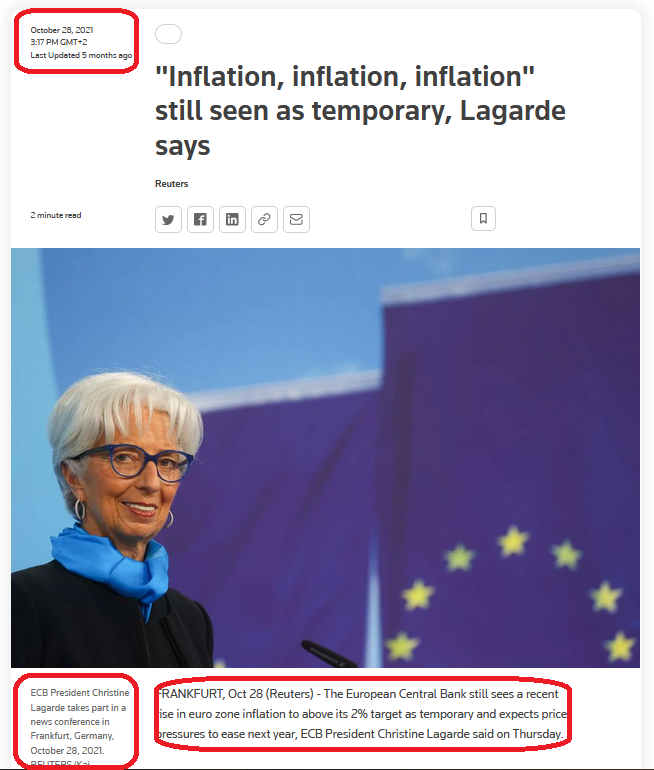

Madame Lagarde, per tutto il 2022 ed in modo insistito, ci ha informati che “dai dati disponibili oggi non si vede alcun rischio di stagflazione”. In modo particolare il 30 marzo 2022 noi abbiamo archiviato l’immagine qui sopra. La abbiamo archiviata nel nostra database, mettendola con cura a fianco dell’immagine che segue, che è datata 28 ottobre 2021. Esattamente cinque mesi prima. Cinque mesi sono 150 giorni circa.

Questi personaggi oggi sono alla guida delle Istituzioni a cui è stato affidato il potere assoluto sulla politica monetaria: per noi investitori, questo è motivo di preoccupazione. Anzi, questo è la massima ragione di preoccupazione, come vi scriviamo da due anni. E come abbiamo ulteriormente ribadito solo ieri nel nostro ultimo Longform’d.

Per fortuna, non tutti i banchieri centrali sono incompetenti ed irresponsabili: solo la maggior parte di quelli oggi in carica (ma passerà anche questa).

Per completezza, vogliamo evidenziare qui che c’è tra i Banchieri Centrali c’è anche chi preferisce, alla propaganda … da venditori di pentole in TV, il parlare con chiarezza e competenza, come la carica richiede.

Qui sotto, noi vi riportiamo le parole di un esponente della Banca di Inghilterra, pronunciate qualche settimana fa.

Si tratta di parole molto utili, per comprendere il contesto che tutti ci troviamo ad affrontare. Sono utili in particolare per i molti che, ancora oggi, si comportano che se l’inflazione fosse un fenomeno virtuale, come se tutto intorno a loro fosse un videogioco, dove è sufficiente premere il tasto “RESET” e tutto si azzera.

Si tratta di molti investitori, di molti operatori economici e pure di molti semplici consumatori, che si atteggiano come se non fosse successo nulla nella vita reale, che si rifiutano di vedere il cambiamento in atto, a proposito del quale è giustificato utilizzare l’aggettivo “storico” come è stato fatto proprio da questo esponente della Banca di Inghilterra.

A tutti questi soggetti, la lettura dell’articolo che segue risulterà particolarmente utile.

Amici lettori: la realtà, quella nella quale ogni giorno lavorate, vi divertite, respirate e mangiate è quella che viene descritta qui sotto. Aprite gli occhi, e fatelo per tempo.

Britons face a “historic shock” to their incomes this year sparked by surging energy prices that will hit UK economic growth and consumer demand, Bank of England governor Andrew Bailey warned on Monday.

Bailey said Russia’s invasion of Ukraine would fuel the UK cost of living crunch, adding the energy price shock in 2022 would be larger than during any single year in the 1970s.

The BoE governor sounded the alarm on so-called stagflation, suggesting slowing economic growth and soaring inflation posed the biggest challenge to the central bank’s Monetary Policy Committee since its creation in 1997. Surging energy prices are a key factor behind UK consumer price inflation reaching a 30-year high of 6.2 per cent in February, more than three times the BoE’s 2 per cent target. The BoE expects Russia’s war in Ukraine to help push inflation to about 8 per cent in the second quarter of this year.

It said this month inflation could potentially climb even higher in the autumn, when regulated energy prices are due to increase further. The shock from energy prices this year will be larger than any single year in the 1970s. Andrew Bailey Bailey said Britons were facing a “very large shock to aggregate real income and spending” from rising prices of energy and imported goods. He told an event organised by Bruegel, the think-tank, in Brussels: “This is really an historic shock to real incomes.” Bailey said Russia’s invasion of Ukraine had exacerbated the energy supply shock, adding: “The shock from energy prices this year will be larger than any single year in the 1970s. The caveat is that the 1970s had a succession of years and we very much hope that would not be the case now. But as a single year, this is a very, very big shock.”

UK inflation spiralled upwards during the 1970s after Arab members of Opec, the cartel of oil producers, imposed a crude embargo on countries that had supported Israel in the Yom Kippur war. Bailey said the UK and the eurozone were confronting a similar energy shock, because they both relied on the same gas market, adding it was different for the US because of its bigger domestic supply. He also said the US was experiencing a stronger rebound in demand after the worst of the coronavirus pandemic compared with the UK and Europe.

Last week, the Office for Budget Responsibility, Britain’s fiscal watchdog, predicted that UK household real income this year would contract at the sharpest rate since records began in the 1950s. Bailey said: “We expect it to cause growth and demand to slow. We’re beginning to see the evidence of that in both consumer and business surveys.” The OBR has cut its UK growth forecast for 2022 from 6 per cent to 3.8 per cent.

Slower economic growth and higher inflation are often referred to as stagflation: a relatively uncommon situation as prices of goods and services tend to rise most sharply in periods of robust consumer demand and strong expansion of output. Bailey said the BoE had a variety of monetary policy tools to deal with the current situation, but warned of the challenges given growth and inflation were “pulling in different directions”. “This is a big trade-off,” he added. “I think it’s the biggest trade-off the Monetary Policy Committee has faced in its now approaching 25 years life.”

Meanwhile chancellor Rishi Sunak told the House of Commons Treasury select committee he was determined to hold down public borrowing and spending, saying he feared that looser fiscal policy could further fuel inflation. Sunak said a 1 percentage point rise in inflation and interest rates could “wipe out” the headroom he had built into his tax and spending plans in the run-up to the next election.

Dopo avere letto queste utili parole del Governatore della Banca di Inghilterra, ora ritorniamo al Giappone ed a Kuroda, dal quale il nostro Longform’d era partito.

E rivediamo nel dettaglio, con l’articolo che segue, la riunione di ieri: riunione di ieri che resterà, a nostro avviso, nella storia dei mercati finanziari tanto quanto la “riunione di emergenza” della BCE del mercoledì 15 giugno e poi la riunione “dello 0,75%” della Federal Reserve del giorno successivo.

Per quale ragione? Lo leggerete nell’articolo, ed in particolare nella parte dell’articolo che Recce’d ha evdenziato per voi.

Following a week of historic rate hikes and aggressive moves by the Federal Reserve and other major central banks, the Bank of Japan has hardly ever seemed more like a rebel standing athwart the consensus.

And after its two-day policy meeting Friday, the BOJ, as expected, left interest rates at ultraloose levels, despite a plunging Japanese yen.

Unfortunately for some investors, the BOJ’s refusal to accede to the market’s demands has come at a price. And judging by recent market ructions in the dollar-yen currency pair , Japanese stocks (which were sinking in Friday trading) and the market for Japanese government debt — which the BOJ has long backstopped with seemingly bottomless bid — it looks like the central bank has found itself entrenched in a battle with foreign speculators, analysts said.

Despite the central bank ramping up its bond-buying earlier in the week, Japanese government bonds, particularly at durations below the 10-year mark, have seen yields, which move opposite of prices, surge.

The selloff cooled on Thursday as the Bank of Japan’s two-day policy meeting got under way, and yet, the damage has largely been done. Bloomberg reported that the Bank of Japan could face “huge losses” on its $4 trillion trove of government bonds should it abandon its easy money policies.

What’s more, the hope among economists and market participants that the Bank of Japan might make a slightly dovish adjustment to its policy of yield curve control caused markets to whipsaw — the dollar-yen currency pair on Thursday appeared headed for its largest two-day correction since March 2020.

Jens Nordvig, the founder and CEO of Exante Data and a longtime currency market guru, noted via Twitter that the scramble to hedge against a more assertive tone from the Bank of Japan has been quite intense.

As far as what that shift might look like, analysts at Japanese banks have been eerily silent, and economists and market strategists looking on from abroad have ventured to speculate that BOJ Gov. Haruhiko Kuroda and his team might eventually ease up on the acceptable yield ranges for JGBs — although there seems to be wide agreement that any kind of substantial move on the central bank’s part on Friday would be extremely out of character.

When it does arrive, it’s possible that the move could look like a widening of the central bank’s acceptable range for the JGB yields for bonds and bills of the shortest maturity through the 10-year. But even this seems relatively modest when viewed in the context of what the rest of the world’s central banks — with the Federal Reserve front and center — appear to be doing.

The surge in JGB yields appears to have abated (at least, for now), and the dollar has staged a notable reversal, weakening more than 2% against the yen Thursday in what was its biggest two-day drop since March 2020. But analysts say the fact remains that the state of the Japanese 10-year yield curve signals that investors are ready to duke it out with the BoJ, as the bank has been buying trillions of dollars’ worth of bonds just to maintain the status quo. If it persists at the current rate, it will have bought some 10 trillion yen (worth some $75 billion) in June.

“This is a truly extremely level of money printing,” said Deutsche Bank’s George Saravelos.

What’s at stake?

Saravelos warned that if confidence in the BOJ’s ultraloose policy gives way, the result could be chaos in Japanese stocks and equities.

“If it becomes obvious to the market that the clearing level of JGB yields is

above the BoJ’s 25 basis point target, what is the incentive to hold bonds any more?” Saravelos said. “Is the BoJ willing to absorb the entirety of the Japanese government bond stock?”

“Where is the fair value of the yen on this scenario and what happens if the BoJ

changes its mind?” he said.

But it’s not just Japan that will be affected — far from it. Analysts said ripples could spread through stock and equity markets across Asia, and perhaps Europe and the U.S. as well.

Further strength in the U.S. dollar accentuates market sensitivities across the world by making life more difficult for emerging market corporations and governments to service their debt. It’s one reason why the rate hiking cycles can sometimes help provoke problems like the “Tequila Crises” of 1994.

Of course, the Bank of Japan wouldn’t want a replay of that either.

How did we get here?

Fortunately for the Bank of Japan, markets are getting a bit of reprieve on Thursday with the weak U.S. economic data coming just before their big rate decision, according to Steve Englander, FX strategist at Standard Chartered Bank.

U.S. jobless claims lingered near five-month highs last week, and housing starts signaled that trouble could be brewing in the U.S. real-estate market (both of which could be construed as positive developments on the Federal Reserve’s agenda).

Japan and the BOJ fought for years to try to push inflation higher and return the Japanese economy to a state of more dynamic growth. Unfortunately, a slew of factors, including demographic issues, has held it back.

Now, the BOJ needs to find the sweet spot where it can accommodate investors demanding a dramatic policy shift, while also not ceding 100% of the control over the narrative to speculators and bond vigilantes.

“The problem with that is once you let go a little bit, the market anticipates that you will let go a lot,” Englander said. “Until you get to a level where the market says ‘this looks reasonable’ they’re going to be facing that pressure.”