Non c'è bisogna di commenti: date voi un senso ai fatti

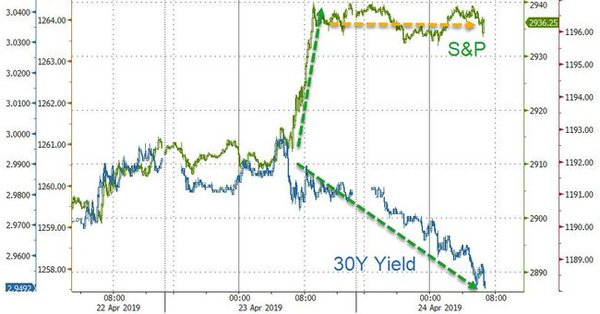

Ieri 24 aprile un movimento violento dei rendimenti obbligazionari, verso il basso, ha spinto nuovamente il rendimento del decennale Bund tedesco sotto lo zero, innescando una reazione di panico nell’intero mercato obbligazionario globale (nel grafico).

Si ripropongono di nuovo gli estremi e le anomalie che abbiamo già commentato nel Blog, e si ripropone il “grafico del coccodrillo” che vedete sopra, il cui significato ormai è chiarissimo a tutti i nostri lettori.

Noi oggi NON faremo ulteriori commenti.

Vi suggeriamo però di leggere con attenzione le parole che seguono, che sono state scritte ieri sul Wall Street Journal e che risultano molto rappresentative del clima che si respira sui mercati di tutto il Mondo. Sono una perfetta sintesi per chi NON la vede come noi.

“Normally, you don’t see that because people interpret lower interest rates as sign of slower growth,” said Donald Ellenberger, senior portfolio manager at Federated Investors. Gains in Treasury prices don’t ordinarily coincide with a climb in values for stocks because government paper is considered a hedge against market uncertainty and sluggish economic growth, while stocks tend to gain in value on hope of healthy expansion.

Ellenberger said, “so the question is why” is this happening? The Federated portfolio manager said there may be a simple explanation for the unusual relationship between bonds and stocks currently in force: “Usually, it means the stock market is expecting strong growth and the bond market is expecting recession and one has to be right and one has to be wrong,” he said. “I don’t think that is the right way to look at it — they are both responding to the Fed,” he said.

Back in January, the Federal Reserve, led by Chairman Jerome Powell, said it was holding off on further rate hikes after delivering four increases in 2019, moves that were widely viewed as contributing to tightening financial conditions, culminating in a violent selloff in late December. The central bank reaffirmed its wait-and-see approach policy pivot in March and said it would end the unwind of its $4 trillion balance sheet, another policy measure that market participants say had unsettled equity investors. The yield on the benchmark 10-year note has retreated from a peak at 3.262% on Oct. 9.

This is “nirvana for stocks” too, Ellenberger said because the Fed has communicated that it might not immediately raise borrowing costs further even if growth accelerates significantly pushing reading of inflation above its 2% target. Powell hinted in congressional testimony earlier this year that he was willing to allow inflation to temporarily overshoot its goal, enabling prices not just to reach 2% in better economic times but to average around that level.

Noi non commentiamo, oggi, queste parole, ma ci sembra molto utile ricordare anche oggi che 1) il mercato finanziario NON è un videogioco; e che 2) investire significa guardare alla realtà ed evitare le fantasie. Il resto, viene da solo, per conseguenza.

Aggiungiamo una cosa: oggi, il mercato è questo. Molto diverso, da dieci, venti, trenta anni fa. Completamente diverso.

Cambiato in meglio? In peggio? Non sta a noi dare giudizi morali.

La soluzione, per evitare questi alti e bassi e questi estremi emotivi, è rinunciare ad investire? Se non si ha tenuta nervosa, se non si ha pazienza, forse sarebbe preferibile.

Ma sarebbe anche un errore: le opportunità di guadagno più grandi della vostra vita, della vostra intera esperienza di investitori, sono proprio lì, oggi, davanti ai vostri occhi. basta un pizzico di pazienza, un po’ di buon senso, e tenere il nervo sotto controllo.