Longform’d. Analisi di un rimbalzo: è anche lui “transitorio”?

Dopo ben otto settimane, la Borsa a New York ha chiuso in rialzo venerdì 27 maggio 2022. Il rialzo settimanale supera il 6%.

Si tratta del fatto del giorno, ed è un argomento inevitabile.

Ma si tratta di un argomento importante, nella logica della gestione di portafoglio? Si tratta di un fatto rilevante? Ci porta a comperare oppure a vendere? Modifica le nostre aspettative per il futuro?

La risposta di Recce’d è NO: a tutte le domande lette qui sopra.

Che cosa fare, lo diremo poi la settimana prossima ai nostri Clienti, nella Sezione Operatività del nostro quotidiano The Morning Brief.

Ma ugualmente, per i lettori del Blog, intendiamo (come sempre facciamo) produrre gratuitamente elementi di valutazione e di giudizio: un contributo concreto ed applicabile per decidere che cosa fare.

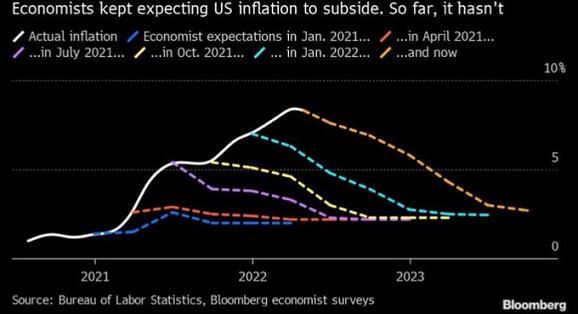

Il rimbalzo, come leggete qui sopra, è stato annunciato più volte: qui si torna addirittura al mese di ottobre del 2021, ovvero si ritorna indietro di ben sette mesi. Leggete nel titolo: “buy-the-dip” è l’indicazione operativa. La motivazione che fu fornita, allora, da Goldman Sachs e JP Morgan, fu questa: “L’inflazione è transitoria”.

Le cose poi non andarono esattamente in quel modo: lo documentiamo con il grafico che segue.

L’inflazione non era “transitoria”, e comperare il tema “buy-the-dip” da Goldman e JP Morgan fu un errore nell’ottobre 2021.

Fu un errore anche in novembre, dicembre, gennaio, febbraio, e marzo e aprile e maggio 2022.

Il tema è rilevante per il semplice fatto che proprio la scorsa settimana … ci hanno riprovato. Il tema però si è trasformato: il suggerimento operativo è sempre “buy-the-dip” ma la scorsa settimana c’era una nuova motivazione, e precisamente quella che “la Federal Reserve farà una pausa il prossimo settembre” . Interromperà il ciclo di rialzi dei tassi di interesse.

Sui mercati finanziari, in questo maggio del 2022, sono in moltissimi quelli che hanno “nostalgia”: vorrebbero tornare ai bei tempi andati, quando le Banche Centrali facevano semplicemente “tutto quello che volevano”.

Quei tempi però sono andati per sempre: non torneranno mai più. Le Banche centrali oggi fanno ciò che sono costrette a fare. Costrette dalla realtà. Oggi, la realtà le ha costrette ad alzare i tassi. Se faranno una pausa, in settembre, non dipende da una loro scelta, ma da ciò che faranno i dati.

Come investitori, quindi, siete costretti a rispondere ad una semplicissima domanda: ci saranno segnali di una inflazione sotto controllo, da qui a settembre?

La risposta di Recce’d verrà consegnata ai nostri Clienti ogni mattina, la settimana prossima, nel The Morning Brief. Oggi nel Longform’d ci limitiamo a ragionare con i lettori di dati e di movimenti di mercato, come il calo dei rendimento sui Titoli di Stato che avete visto la settimana scorsa (e che ha sostenuto il rimbalzo delle Borse).

Un movimento come quello che vi documentiamo qui sopra, nell’immagine, giustifica una previsione di “peak rates”, ovvero che i tassi di interesse abbiamo già raggiunto il loro massimo del 2022 (almeno, per le scadenze lunghe come i 10 anni)?

Ovviamente, la domanda è complessa, e la risposta richiede competenza e capacità di analisi. I numeri sono essenziali, in analisi di questo tipo: è importante evitare le trappole emotive, è importante evitare di affidarsi a “sensazioni” ed “emozioni”, è importante guardare invece con attenzione ai numeri.

Un veterano di Wall Street come Stephen Roach lo ha fatto, e poi ha pubblicato l’articolo che segue, dove si esprimono opinioni molti vicine a quelle di Recce’d. Roach indica la misura dei rialzi dei tassi che oggi è necessaria per incidere sull’epidemia di inflazione: ci dice in altre parole di quanti punti percentuali Powell dovrà alzare i tassi se vuole vedere “peak inflation” e “peak rates”.

Da una analisi di questo tipo, si può ricavare una risposta alla domanda di cui dicevamo sopra: i rendimenti delle obbligazioni hanno già raggiunto il loro massimo per il 2022?

NEW YORK, May 26 (Reuters) - The Federal Reserve could pause its monetary policy tightening in September if there is an economic deterioration and inflation subsides, BofA strategists said on Thursday, a day after the U.S. central bank released the minutes from its May policy meeting.

All of the Fed's policymakers agreed to hike interest rates by half a percentage point at the May 3-4 policy meeting to counter rampant inflation and most participants said further hikes of that magnitude in June and July could be appropriate.

But the minutes also showed the Fed grappling with how best to reduce inflation without causing a recession or pushing the unemployment rate substantially higher - a task that several participants said would prove challenging. read more

The central bank would likely pause its tightening in September, leaving its benchmark overnight interest rate in a range of 1.75% to 2% if financial conditions worsened, BofA strategists said in a note.

"We have recently seen a tenuous but remarkable change in Fed communications, where some Fed officials suggest the option of downshifting or pausing later in the year as they reach 2% given the challenging macro backdrop, tightening of financial conditions, and potentially softening inflation," they said.

Inflation, by the Fed's preferred measure, is currently running at more than three times the central bank's 2% target.

Fed funds futures traders on Thursday were pricing in 50-basis-point rate hikes at each of the central bank's June and July meetings and another 25-basis-point hike in September. FEDWATCH

While noting that it was not its base case scenario, BofA said the central bank may see a federal funds rate at 1.75%-2% as providing "a normalization of policy which then offers an opportunity to pause and assess the impact on jobs and inflation."

A pause in tightening could lead to lower rates across the U.S. Treasury yield curve, the strategists said.

The benchmark 10-year U.S. government bond yield hit its lowest level since April on Thursday. It has fallen from 3.2% on May 9, as the bond market sees the economy slowing and expects inflation to lose momentum.

Other analysts, however, do not see the Fed as having shifted to a more dovish stance.

Strategists at TD Securities said they expected the central bank to hike rates above the neutral rate, the level which neither stimulates nor constricts economic growth, but at a more gradual pace after the June and July policy meetings. Fed policymakers estimate the neutral rate to be roughly between 2% and 3%.

"The views expressed in the minutes are about all they could say at the start of an aggressive tightening cycle where no one really knows how far rates have to go," investment bank Brown Brothers Harriman said in a note.

"The Fed is facing a very complicated situation and so is trying to burnish its hawkish credentials while trying not to pre-commit to any rate path", it said.

If the US Federal Reserve wishes to avoid a return to stagflation, it must recognize the huge gulf between the level of real interest rates under former Fed Chair Paul Volcker and the current incumbent. It is delusional to think that today’s wildly accommodative monetary policy can solve the worst inflation problem in a generation.

Poor Jerome Powell. With US inflation close to a 40-year high, the Federal Reserve chair knows what he needs to do. He has professed great admiration for Paul Volcker, his 1980s-era predecessor, as a role model.

But, to paraphrase US Senator Lloyd Bentsen’s famous 1988 quip about his vice-presidential rival, Senator Dan Quayle, I knew Paul Volcker very well, and Powell is no Paul Volcker.

Volcker was the quintessential US public servant. He smoked cheap cigars, wore rumpled off-the-rack suits, and had a strong distaste for the glitz of Washington power circles. His legacy was a single-minded discipline in attacking a pernicious Great Inflation.

Unlike the modern Fed, which under Ben Bernanke’s intellectual stewardship created a new arsenal of tools – balance-sheet adjustments, special lending facilities, and the “forward guidance” of outcome-dependent policy signals – the Volcker approach was simple, blunt, and direct. Monetary policy, in Volcker’s view, started and ended with interest rates. He once said to me, “If you are not prepared to act on interest rates, you may as well get out of town.”

Volcker, of course, raised US interest rates to unheard-of levels in 1980-81, and there were many who did want him to get out of town. But howls of protest from builders, farmers, citizens’ groups, and members of Congress demanding his impeachment did not dissuade him from an unprecedented tightening in monetary policy.

It was long overdue. Under Volcker’s predecessor, Arthur Burns, the Fed had become convinced that inflation was part of the US economy’s institutional fabric. The price level was thought to have less to do with monetary policy than with the power of labor unions, cost-of-living wage indexation, and regulatory pressures on costs stemming from environmental protection, occupational safety, and pension benefits. Burns argued that oil and food-price shocks reinforced the institutional biases of an inflation-prone US economy. In other words, blame the system, not the Fed. The Fed’s research staff, which at the time included me, squirmed but raised no objections.

Volcker did more than squirm when he took over as Fed chair in August 1979. At the time, the consumer price index was surging by 11.8% year on year, on its way to 14.6% in March 1980. Volcker was determined to find the interest-rate threshold that would break the back of US inflation. Using the political cover provided by the 1978 Humphrey-Hawkins Act, which formalized the Fed’s price-stability mandate, and drawing operational support from a shift to targeting the money supply, Volcker went into action.

The Fed increased its benchmark federal funds rate from 10.5% in July 1979 to 17.6% in April 1980. Volcker then reversed course during an ill-advised but short-lived experiment with credit controls in the spring of 1980, before resuming a monetary-policy tightening that eventually pushed the funds rate to a monthly peak of 19.1% in June 1981. Only then did the fever of double-digit inflation break.

By late 1982, with the US in deep recession, annual headline CPI inflation had slipped below 4%, and the Fed started to reduce the benchmark policy rate. Mindful of the deeply entrenched inflationary psychology still gripping America, the Fed moved slowly and cautiously. Volcker, having broken the back of inflation, was not about to “leave town” until the Fed’s mission was complete.

Fast-forward 40 years, and Powell’s problem is glaringly apparent. Yes, the world today is certainly different than it was back then. But the modern Fed apparently has no institutional memory of the mistakes that it made in the Burns era. In 2021, there was a striking sense of déjà vu when US central bankers treated the initial surge in inflation as transitory and squandered the credibility of well-anchored expectations of low inflation.

The Fed viewed the COVID-19 shock in the same way it viewed the global financial crisis of 2008-09, and injected massive monetary stimulus to address what it was convinced would be a protracted shortfall in aggregate demand. In retrospect, that was an epic policy blunder. As pandemic-related lockdowns quickly gave way to a reopening of the economy, aggregate demand, aided by massive fiscal stimulus, snapped back with a vengeance. And in the face of now seemingly chronic supply-chain disruptions, this post-lockdown takeoff spawned the great inflation of our generation.

Powell’s problem is all the more evident when viewed through the inflation-adjusted lens of real interest rates. Over the 51 months of his leadership of the Fed (through April 2022), the real federal funds rate has averaged -1.95% (with a stress on the minus sign). This extraordinary monetary accommodation is unmatched in modern times. The real funds rate averaged -0.05% for eight years under Burns, -0.7% during Bernanke’s eight-year tenure, and -0.9% for four years under his successor, Janet Yellen.

Under Volcker, by comparison, the real federal funds rate averaged 4.4% for eight years (with a stress on the positive sign). Moreover, notwithstanding the Powell Fed’s newfound determination to move swiftly to counter what it belatedly views as a serious inflation problem, I suspect that the federal funds rate will remain below the US inflation rate well into 2023. That would push the Powell average down to -2.25% over the 59 months ending in December 2022.

No, I am not arguing that Powell needs to replicate Volcker’s tightening campaign. But if the Fed wishes to avoid a replay of the stagflation of the late 1970s and early 1980s, it needs to recognize the extraordinary gulf between Volcker’s 4.4% real interest rate and Powell’s -2.25%. It is delusional to believe that such a wildly accommodative policy trajectory can solve America’s worst inflation problem in a generation.

Like Volcker, Powell takes his mission of public service very seriously. Unfortunately, as Bentsen might have said, that is where the comparison ends

L’analisi di Stephen Roach che avete appena letto è completa ed esaustiva, per ciò che riguarda il tema del costo ufficiale del denaro e dei tassi di interesse. Noi gestori di portafoglio però dobbiamo ogni giorno guardare all’insieme del portafoglio titoli, ovvero a tutte le sue componenti: azioni, obbligazioni, materie prime e valute.

Il tema dei tassi di interesse, da solo, non ci permette di guidare con consapevolezza la strategia di investimento: lo dobbiamo unire ad altri temi, sui quali è necessario un quotidiano aggiornamento. Forniremo, ai nostri lettori, alcuni esempi.

Il tema dei tassi e dell’inflazione si interseca, prima di tutto, con il tema della crescita economica: nel grafico che trovate di seguito, si vede che i dati economici pubblicati nel 2022 per l’economia degli Stati Uniti sono stati, regolarmente, inferiori alle previsioni, ed in una misura crescente con il passare delle settimane.

I dati macroeconomici in arrivo dalla Cina e dall’Europa, nel 2022, sono stati anch’essi regolarmente inferiori alle previsioni. Questo ha determinato nel corso del 2022 una ampia revisione delle previsioni anche per i prossimi mesi.

Lo scenario che ci viene prospettato, oggi, è quindi uno scenario di bassa crescita delle economie, e di elevata inflazione: si chiama STAGFLAZIONE ed è proprio lo scenario sul quale noi di Recce’d avevamo chiamato la vostra attenzione dall’estate del 2020 e per tutto il periodo successivo.

I banchieri centrali, fino ad oggi, hanno tenuto una linea che, di fatto, nega la possibilità di stagflazione e si concentra sulla eventualità del “soft landing”, pur essendo costretti a riconoscere che “ci saranno ricadute negative”, come fece la settimana scorsa Jerome Powell e come ci spiega James Bullard nell’intervento che riportiamo sotto..

Retailers who endlessly raise their prices and don’t understand that consumers are stretched thin because of inflation are going to lose market share, said St. Louis Fed President James Bullard on Friday.

“A lot of CEOs have come on TV and said ‘oh I have lots of pricing power and I can do whatever I want and make a lot of money’,” Bullard said Friday, in an interview on the Fox Business Network.

“But I think some of them are going to get punched in the face here with the fact that consumers have to react” to higher inflation, he said.

Households only have so many dollars coming into their bank accounts and they have to decide what to buy. They are going to choose the basic necessity rather than the luxury good, Bullard added.

This dynamic will help inflation moderate, Bullard said.

In the interview, Bullard gave no indication that the stock market selloff this month had caused him to waver in his support for half-a-percentage point rate hikes at the Fed’s next two meetings in June and July.

Those two moves would lift the Fed’s benchmark fed funds rate up to a range of 1.75-2% by August.

“50 basis points is a good plan for now,” he said.

“We have to get inflation under control and I think we have a good plan to do so,” Bullard said.

Some of the repricing in the equity market might be due to the Fed, but other factors were also at play, he said.

Bullard said he still would like to see the Fed raise its benchmark interest rate up to 3.5% by the end of the year. That’s a more aggressive path than most of his colleagues are sketched out.

The St. Louis Fed president said getting up to a 3.5% rate might possibly allow the central bank to lower rates in 2023 or 2024.

Bullard downplayed fear of a recession or stagflation.

Stagflation means a recession with inflation continuing to move higher, he said.

“I don’t see that as a scenario right here,” Bullard said. In fact, he predicted U.S. economic growth will be stronger after June than it was in the first six months of the year.

And Bullard said it would take a “big shock” to push the U.S. into a recession and he doesn’t see that on the horizon.

Le parole di Bullard che abbiamo riportato qui sono di una particolare rilevanza, a giudizio di Recce’d, nella parte dove si parla delle politiche di prezzo delle aziende: dice Bullard che “prenderanno un pugno in faccia quelle aziende della distribuzione che non capiscono che i consumatori spendono meno”.

In pratica, Bullard afferma che le Aziende devono capire di non avere tutto quello spazio per alzare i prezzi, e che devono “tenersi in casa” una parte delle ricadute degli aumenti di prezzo.

Ciò che ci porta immediatamente ad un altro dei temi che oggi vogliamo segnalare: il rema degli utili.

Se le Aziende sceglieranno di non scaricare l’inflazione per intero sul Cliente, gli utili delle Società ne soffriranno.

Per noi investitori, questo significa una di queste due conseguenze: prezzi più bassi per le azioni, oppure valutazioni più elevate sulla base di utili più bassi.

Le grandi banche di investimento si sono già mosse, nel modo che vedete sopra nel grafico: hanno abbassato le stime per il valore della Borsa a fine 2022, ma hanno mantenuto ferme le stime per gli utili delle Società (le stime che nel grafico vengono chiamate EPS, ovvero utile-per-azione).

Il grafico qui sopra, che è di una decina di giorni fa, è interessante per almeno due ragioni:

il nuovo target di Goldman Sachs, per dicembre, è di 4300 punti per l’indice S&P 500; ma se per effetto del rimbalzo dell’ultima settimana siamo ritornati a 4150 punti circa. Questo allora significa che da qui ai prossimi sette mesi tutto si ferma?

e poi: gli utili per azione rimangono, come vedete, ai massimi di sempre secondo Goldman, anche nel 2022: e quindi, le cose di cui parlava Bullard più sopra semplicemente … non esistono?

Ecco uno dei fattori che devono orientare le vostre scelte di investimento.

Con questi pochi, e selezionati esempi, Recce’d vuole aiutarvi a capire che il rimbalzo di una settimana, basato sul tema “pausa di settembre e peak rates”, è soltanto un dettaglio in una storia che è molto più ampia e molto più complessa.

Per questo, più in alto abbiamo risposto NO alla domanda se questo rimbalzo è rilevante, per la nostra strategia di investimento e per la gestione di portafoglio. Un buon gestore di portafoglio guarda anche ad altri fattori, e li esamina tutti insieme per costruire uno scenario coerente per i propri investimenti.

Alcuni fattori ve li abbiamo già esposti: per chiudere, ne citiamo un altro, che è la storia dei mercati finanziari: e più nello specifico, la storia dei rimbalzi. Ad esempio dei rimbalzi tra il 2000 ed il 2003, che vi raccontiamo con il grafico qui sotto

La storia non si ripete, ma spesso fa rima, come disse lo scrittore Mark Twain.

La conclusione di questo nostro Longform’d è un suggerimento al lettore: per gestire in modo attivo e produttivo i propri investimenti, è un errore affidarsi agli slogan ed alle dichiarazioni. Lo è sempre, ma in modo particolare lo sarà in questo 2022, un anno che già oggi è molto diverso da quello che tutti immaginavano ad inizio anno, e che a fine 2022 sarà ancora più distante dalle previsioni della massa.

Molte sorprese sono già arrivate, ed altre sono in arrivo: il nostro suggerimento è di preparare i vostri portafogli.

Reagiste alle parole, come sempre rassicuranti e zuccherose, dei banchieri centrali e del vostro promotore finanziari: non ci sarà nessun “soft landing”, ed accadranno invece cose che voi, e loro, neppure immaginate, in questo 2022.

Nell’articolo che chiude il Longform’d, si spiega in modo chiarissimo perché lo scenario di “soft landing” oggi è esattamente la medesima cosa che sei mesi fa era “l’inflazione transitoria” di cui abbiamo scritto più sopra.

Fermatevi a fare due conti: che cosa sarebbe cambiato per i vostri soldi, sei mesi fa, se sei mesi fa voi aveste dato ascolto ai suggerimenti di questo Blog e modificato il vostro portafoglio di investimenti?

Oggi si ripete proprio quella situazione.

After more than a decade of chained stimulus packages and extremely low rates, with trillions of dollars of monetary stimulus fuelling elevated asset valuations and incentivising an enormous leveraged bet on risk, the idea of a controlled explosion or a “soft landing” is impossible.

In an interview with Marketplace, Federal Reserve chairman admitted that “a soft landing is really just getting back to 2% inflation while keeping the labor market strong. And it’s quite challenging to accomplish that right now”. He went on to say that “nonetheless, we think there are pathways … for us to get there.”

The first problem of a soft landing is the evidence of the weak economic data. While headline unemployment rate appears robust, both the labor participation and employment rate show a different picture, as they have been stagnant for almost a year. Both the labor force participation rate, at 62.2 percent, and the employment-population ratio, at 60.0 percent remain each 1.2 percentage points below their February 2020 values, as the April Jobs Report shows. Real wages are down, as inflation completely eats away the nominal wage increase. According to the Bureau of Labor Statistics, real average hourly earnings decreased 2.6 percent, seasonally adjusted, from April 2021 to April 2022. The change in real average hourly earnings combined with a decrease of 0.9 percent in the average workweek resulted in a 3.4-percent decrease in real average weekly earnings over this period.

The University of Michigan consumer confidence in early May fell to an 11-year low of 59.1, from 65.2, deep into recessionary territory. The current conditions index fell to 63.6, from 69.4, but the expectations index plummeted to 56.3, from 62.5.

The second problem of believing in a soft landing is underestimating the chain reaction impact of even allegedly small corrections in markets. With global debt at all-time highs and margin debt in the US alone at $773 billion, expectations of a controlled explosion where markets and the indebted sectors will absorb the rate hikes without a significant damage to the economy are simply too optimistic. Margin debt remains more than $170 billion above the 2019 level, which was an all-time high at the time.

However, the biggest problem is that the Federal Reserve wants to curb inflation while at the same time the Federal government is unwilling to reduce spending. Ultimately, inflation is reduced by cutting the amount of broad money in the economy, and if government spending remains the same, the efforts to reduce inflation will only come from obliterating the private sector through higher cost of debt and a collapse in consumption. You know that the economy is in trouble when the fiscal deficit is only reduced to $360 billion in the first seven months of fiscal year 2022 despite record receipts and the tailwind of a strong recovery in GDP. Now, with GDP growth likely to be flat in the first six months but mandatory and discretional spending still virtually intact, government consumption of monetary reserves is likely to keep core inflation elevated even if oil and gas prices moderate.

The Federal Reserve cannot expect a soft landing when the economy did not even take off, it was bloated with a chain of newly printed stimulus packages that have made the debt soar and created the perverse incentive to monetize all that the Federal government overspends.

The idea of a gradual cooling down of the economy is also negated by the reality of emerging markets and European banks. The relative strength of the US dollar is already creating enormous financial holes in the assets of a financial system that has built the largest carry trade against the dollar in decades. It is almost impossible to calculate the nominal and real losses in pension funds and the negative result of financial institutions in the most aggressively priced assets, from socially responsible investment and technology to infrastructure and private equity. We can see that markets have lost more than $7 trillion in capitalization in the year so far with a very modest move from the Federal Reserve. The impact of these losses is not evident yet in financial institutions, but the write-downs are likely to be significant into the second half of 2022, leading to a credit crunch exacerbated by rate hikes.

Central banks always underestimate how quickly the core capital of a financial institution can dissolve into nonexistence. Even the financial system itself is unable to really understand the complexity of the cross-asset impact of a widespread slump in extremely generous valuations throughout all kinds of assets. That is why stress tests always fail. And financial institutions all over the world have abandoned the healthy process of provisioning expecting a lengthy and solid recovery.

The Federal Reserve tries to convince the world that rates will remain negative in real terms for a long time, but borrowing costs globally are surging while the US dollar is strengthening, creating an enormous vacuum effect that can create significant negative effects on the real economy before the Federal Reserve even realizes that the market is weaker than they anticipated, and liquidity is significantly lower than they calculated.

There is no easy solution. There is no possible painless normalization path. After a massive monetary binge there is no soft hangover. The only thing that the Federal Reserve should have learnt is that the enormous stimulus plans of 2020 created the worst outcome: stubbornly high core inflation with weakening economic growth. There are only two possibilities: To truly tackle inflation and risk a financial crisis led by the US dollar vacuum effect or to forget about inflation, make citizens poorer and maintain the so-called bubble of everything. None is good but they wanted a decisive and unprecedented response to the pandemic lockdowns and created a decisive and unprecedented global financial risk. They thought money creation was not an issue and now the accumulated risk is so high it is hard to see how to tackle it.

One day someone may finally understand that supply shocks are addressed with supply-side policies, not with demand ones. Now it is too late. Powell will have to choose between the risk of a global financial meltdown or prolonged inflation.