Orizzonti di gloria (parte 1)

Il film di Stanley Kubrick che citiamo con il nostro titolo di oggi ci serve per richiamare un'atmosfera di guerra che va ben al di là delle tariffe e coinvolge tutti i mercati finanziari, come abbiamo dettagliato ai Clienti ogni mattina attraverso il nostro The Morning Brief, guida che dimostra tutta la sua utilità giorno dopo giorno, ma in modo particolare quando ... non ci si capisce più nulla, come ad esempio in questo 2018.

Recce'd come tutti ormai sapete guarda con grande interesse al processo di normalizzazione dei mercati iniziato in gennaio, processo che potrebbe accelerare in estate. The Morning Brief da lunedì scorso ha messo in evidenza tutte le (sempre più ampie) divaricazioni e contraddizioni che vediamo sui mercati finanziari, e una soluzione dovrà necessariamente arrivare.

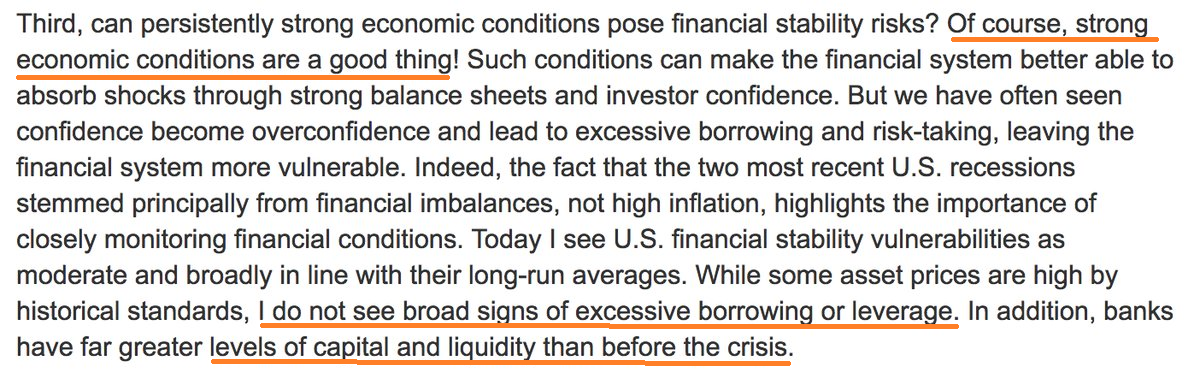

Oggi nel Blog commentiamo la più grande di tutte. Partendo dalle parole del Chairman Powell ieri a Sintra, che rileggete qui di seguito.

Notate bene le tre cose evidenziate: 1) la grande fiducia nell'economia (è importante il tono: non la realtà dei fatti) 2) il rifermento al grandi di indebitamento o "leverage" e 3) il riferimento al capitale delle banche

Tre punti che meritano un commento:

- Powell sa perfettamente che questo ritmo di crescita dell'economia USA NON durerà nel tempo, come lo sappiamo tutti; in questo preciso momento, però, la Fed ha BISOGNO di alzare i tassi ufficiali (per avere in futuro margini di manovra)

- il "leverage" era il drammatico problema della Grande Crisi 2007-2009; ma ciò che Powell non dice, e nessuno dei suoi lo dice, è che il problema NON è mai stato risolto; è stato soltanto SPOSTATO, sui mercati finanziari: oggi c'è meno debito bancario rispetto al 2007, ma c'è molto più debito ottenuto emettendo obbligazioni; e NON è meno pericoloso, come ha spiegato anche di recente Goldman Sachs che citiamo più sotto

- il capitale delle banche è adeguato ai rischi? lo sapremo soltanto quando i rischi si saranno presentati, un test ancora non lo abbiamo visto (grazie al soccorso prolungato, insistito, e smodato delle Banche Centrali, che ora però sta rientrando)

Per voi investitori, delle tre osservazioni proposte quella che avrà il peso maggiore, e decisivo, è la seconda: dovete riflettere bene sul fatto che, come ha scritto Goldman, "liquidity is the new leverage". Tema che si lega direttamente ad altri trattati dal nostro Blog di recente. Leggiamo insieme Goldman:

(...) one more prominent strategist has joined the fray, none other than Goldman's head of global credit strategy, Charlie Himmelberg, who in the aftermath of last month's VIXplosion, asks today if "liquidity" itself has become the new market leverage - that critical leading indicator which historically has flashed red ahead of an imminent crash, and which the Fed still uses -erroneously - to guide its macroprudential decisions.

This is how Himmelberg introduces his - far less tinfoil hatted - readers, i.e., those institutional clients who still believe that the market is working as it was designed, as a liquid, efficient, discounting mechanism, to the premise that everything they know is false:

Where is there complacency in this expansion? And where might complacency be hiding unappreciated risks that will be exposed when the expansion ends or the bull market turns? We see clues in Monday, Feb. 5, when the VIX had its largest one-day move in its history, jumping from 17.31 to 37.32, a move of 20 VIX points. Like previous “flash crashes” in other markets over the post-crisis period, there was nothing in the fundamental data to explain a jump of this magnitude. Instead, we think the VIX spike was primarily a reflection of technical trading dynamics. We suspect the Feb. sell-off is symptomatic of a broader risk, namely, the rising “financial fragility” during the post-crisis period. By “fragility” we mean price volatility that arises not from changes in the fundamental outlook for markets, but rather from markets themselves.

Here Goldman's analyst notes that while various conventional indicators of market liquidity like bid-ask spreads suggest that liquidity conditions have been reasonably good during the post-crisis era, he warns that Goldman is starting to see "several reasons to worry that “markets themselves” are becoming a bigger source of market risk than fundamentals."

In particular, new regulations and new technologies have caused a dramatic evolution of the post-crisis ecosystem for providing trading liquidity. In this new market structure, machines have replaced humans, and speed has replaced capital. While such changes have greatly reduced the need for equity capital, and are thus efficiency-enhancing, the same was also true about leverage and structured products during the run-up to the

financial crisis. While the new ecosystem for providing market liquidity has arguably freed up equity capital for more efficient uses, it has also depleted the pools of capital that will be available for liquidity when the cycle turns.