2021: l'anno che risolve (parte 3)

Oggi Recce’d pubblica sei nuovi Post. Il lancio della nuova impostazione di questo Blog (a temi, e con un nuovo layout) è stato rinviato al secondo trimestre 2021 in ragione della rapidissima evoluzione della situazione dei mercati finanziari nel mese di gennaio. Per noi di Recce’d, sono sempre i mercati a dettare i tempi. In aggiunta, oggi le occasioni per gli investitori sono le più grandi di una generazione. e noi di certo non vogliamo perderle di vista.

Sopra, una testimonianza del clima che si respirava la sera del venerdì 19 febbraio 2021 su tutti i mercati delle obbligazioni. Colpisce l’utilizzo della parola “panico”.

Ma come, gli amici alla Federal Reserve non avevano tutto-tutto-tutto sotto controllo?

Più e più volte, abbiamo scritto in questo Post che la realtà alla fine prevale sempre sulle fantasie assortite che leggiamo (noi come voi) ogni giorno sui quotidiani ed ascoltiamo ogni giorno dalla televisione. Non è sufficiente annunciare il 9 novembre 2021 che “è arrivato il vaccino, problema risolto”, se poi la realtà impone tutta una serie di (complessi) passaggi intermedi. Allo stesso modo non è sufficiente annunciare che “tra 6-12 mesi tutto sarà tornato come prima” se non si hanno (neppure lontanamente) le capacità di anticipare i molteplici effetti, alcuni dei quali indesiderati, delle scelte fatte nel 2020.

Ad esempio: la Federal Reserve dice “manterremo i tassi di interesse a zero almeno per altri due anni”, ma la Federal Reserve non è onnipotente. Soltanto gli ingenui possono credere, dopo avere visto ciò che è accaduto sui mercati finanziari tra il 2000 ed il 2020, che le Banche Centrali possano davvero “guidare” i mercati finanziari. Soltanto un bambino può credere che le Banche Centrali possano comunicare in anticipo al pubblico degli investitori dove andranno gli indici di mercato, e quindi quale risultato gli investitori faranno con i loro portafogli titoli.

Il pubblico degli investitori ama farsi cullare da questo tipo di illusioni. Ed ama sognare ad occhi aperti: ecco perché, almeno per un certo periodo, le favole hanno successo.

Poi, arrivano le perdite.

Dal primo giorno del 2021 al 20 febbraio, un portafoglio obbligazionario (Titoli di Stato) in dollari USA ha perso, in media lo 1,625% (pur avendo già guadagnato un sesto della cedola annuale. per quanto bassa). Lo vedete nel grafico che segue).

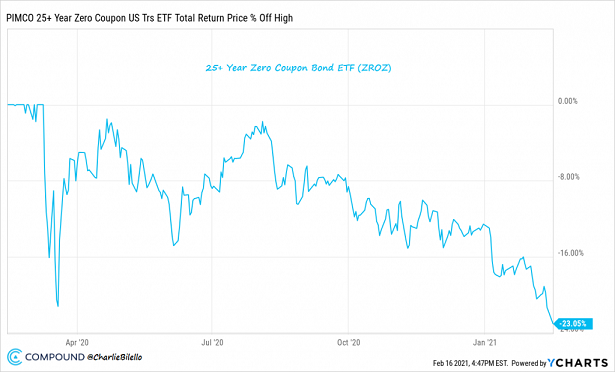

La parte lunga della curva, ovvero i titoli a lunga scadenza (sopra i 25 anni) ha perso un quarto del valore in dieci mesi (-23%). Non stiamo parlando di Gamestop, di Tesla, del Bitcoin: stiamo parlando di Titoli di Stato. Stiamo parlando di obbligazioni: “una sicurezza”, sulla base di ciò che vi aveva raccontato il vostro private banker ovvero promotore finanziario ovvero “consulente” ovvero wealth manager pagato a retrocessioni sui Fondi Comuni che riesce a piazzarvi.

In Europa, i danni sono paragonabili (e già questo, amici lettori, è un qualche cosa sul quale a voi sarebbe utile riflettere).

Ora, sia detto chiaramente che le Banche Centrali non resteranno con le mani in mano: sicuramente interverranno.

Tuttavia, sarà utile ricordare sempre quel detto che dice “quando sei caduto in un buco, c’è una cosa sola cosa da fare: smetti di scavare”.

La Banche Centrali interverranno di sicuro, ancora e sempre con le medesime modalità. Ma è evidente che queste mosse potranno soltanto rendere il buco più profondo. Il buco nel quale, come vedete, sono già caduti anche numerosi investitori.

Il brano che segue vi aiuterà a ricordare che il 2021 potrebbe fare la storia: potrebbe essere l’anno peggiore di tutta la sua storia per il mercato delle obbligazioni.

Invece di divertirvi sullo smartphone oppure sul tablet a cercare notizie su Robinhood e Gamestop, sull’oro e sui nuovi collocamenti (IPOs) potreste cercare voi stessi di rispondere alla domanda che sta proprio in fondo all’articolo che noi vi proponiamo qui di leggere. E’ decisamente più importante, proprio per voi, e per i vostri investimenti.

Noi, sempre allo scopo di renderci utili per i nostri lettori, in modo del tutto gratuito vi aiutiamo più in basso a fornire la risposta giusta.

Over the past 40 years, bond yields have largely moved in one direction: down. The 10-Year Treasury went from a yield of 15.84% in 1981 to an all-time closing low of 0.52% in 2020.

This has been a blessing for bond investors as prices move inversely to yields. And over the last 2 years, as yields plummeted to historic lows, bond investors have experienced extraordinary gains.

But that was the past. What has served as a tailwind for decades (falling rates) is now a major headwind. For there is simply no escaping bond math in which lower yields portend lower future returns.

And with a 10-year treasury yield of 0.92% to start the year, it wouldn’t take much of an increase to make this the worst year for bonds in history (-2.9% in 1994).

We’re on pace for that right now as the 10-year yield has moved up to 1.30% and US bonds are down 1.6% year-to-date.

With a duration of roughly 6 years, a 100 bps (1%) increase in yields would lead to a decline of 6% in aggregate bond prices.

The longer the duration, the larger the decline in yields. We have seen this play out in the long-term zero coupon bond ETF ($ZROZ) which is down over 23% from its high last March (its duration: 27 years).

What could cause bond yields to continue to rise from here?

Che cosa potrebbe da qui in poi spingere ancora verso l’alto i rendimenti delle obbligazioni? Qualche idea ce la potrebbero forse fornire gli indici PMI pubblicati ieri 19 febbraio 2021 negli Stati Uniti (immagine qui sotto) ma sarebbe azzardato affidarsi ad un unico dato.

Tra le centinaia di possibili risposte, che noi abbiamo letto soltanto nell’ultima settimana, (in forma di analisi, commenti, e post sui social media più alla moda) noi abbiamo selezionato per voi un articolo apparso sul Financial Times di venerdì 19 febbraio 2021.

Regaliamo questo lavoro ai lettori, che ci troveranno come sempre disponibili ad approfondire, e soprattutto a tradurre in pratica (gestione del portafoglio) queste preziose indicazioni.

Noi abbiamo lavorato per evidenziare i passaggi essenziali: che vi aiuteranno a comprendere due cose:

perché è sbagliato a dare fiducia a chi vi dice “i tassi salgono perché ci sarà più inflazione”, oppure “i tassi salgono perché ci sarà più crescita economica”

perché vi sarà utile, per non dire indispensabile, ricordare ciò che Recce’d scrisse della cosiddetta “repo crisis” del settembre 2019

Settembre 2019: sei mesi prima del “COVID-19”.

“Beware the Ides of March” (Julius Caesar, act one scene two) Everybody seems to be having a hard time finding the most tradeable forms of dollar cash. In the financial markets this has led to a shortage of T-bills, the form of issuance that can be most readily used as collateral for other trades. As Zoltan Pozsar of Credit Suisse says: “The long, three-year period of front-end collateral glut, which lasted from 2018 [to the beginning of February] is over.”

At the other end of dollar asset respectability, the Fed has ordered a record amount of $100 bills to be printed. At the high end of its estimates, that will be nearly $320bn of $100s — enough for every man, woman and child in the US to have another thousand dollars in ready cash. Of course the C-notes are not going to American civilians — at least 80 per cent are shipped from the bureau of printing to non-US banks.

The dollar is mocked by the well informed, but aggressively hoarded by the fearful, and those who do business in the shadows. Financial panics, especially the ones that do not trigger broad economic recessions, can be useful for some. Coming out of ‘nowhere’, they force markets and politicians to pay attention to excesses that have been excused and problems that have been ignored. Random financial speculation and party politics are at least momentarily set aside so that some unpopular, complicated or unfamiliar changes can be agreed.

The last two weeks of this coming March look like a set-up for some sort of panic in the US Treasury and mortgage-backed securities markets. Not the end of the world, but something like being a passenger in an aircraft that suddenly drops several thousand metres. The most salient and immediate signal to me has been the plunge in short-term Treasury bill rates since the beginning of the year. In the first six weeks of 2021, one-month T-bill rates have fallen by more than 66 per cent. The yield of two-year Treasuries declined by more than 21 per cent.

Those are more dramatic moves than you see in any other broadly traded securities. Unlike the Fed’s favourite instrument, bank ‘excess reserves’ on deposit with the central bank, T-bills are ‘collateral’. They can be readily lent and relent to secure other, unrelated transactions. When people or institutions in the global financial system are not feeling eager to trust each other, they demand more collateral. The degree of that distrust appears to be rising, quickly.

You can see that by looking not only at the outcome of official T-bill auctions, but at the range of bids in the auctions. Low bids mean that dealers are willing to accept very low rates, as little as 1 basis point recently, just to make sure they get some of that collateral. That historically happens at systemic stress points. Simultaneously, the supply of T-bills is shrinking. Because the Treasury wants to rebalance its issuance, it is redeeming bills and selling more long-dated bonds.

That explains part of this year’s unexpected rise in 10-year and 30-year bond yields, which in the past week sailed past the 1.25 per cent level. This in turn triggered a wave of hedging activity by leveraged mortgage banks. As interest rates rise, fewer of the mortgages they own are refinanced at lower rates, and so the “duration” of their assets increases. To offset this ‘convexity’ risk, they have to sell the equivalent of tens, or even hundreds, of billions in Treasury bond derivatives. This is reinforcing the sell-off in Treasuries and threatening a ‘convexity spiral’ of the sort not seen since 2003.

Oh, and the increased derivatives activity needs to be collateralised by T-bills, which you will recall are already in short supply. If my guess is right, then we have the makings of another ‘event’ like we saw a year ago. Market freezes have a way of happening in March and September, an echo of the crop cycle. That might make it momentarily easier to get past the politics of raising the ‘debt ceiling’. And the big banks might get one more year’s waiver on shrinking their asset base.